Executive Summary

The current bull market has been driven mostly by valuation expansion; now valuation is historically high. We expect earnings growth to perpetuate the bull market this year; any more valuation expansion could leave the market vulnerable to a meltdown. Our year-end target for the S&P 500 is 7000, based on a solid rise in earnings with no further valuation expansion. … Much of our optimism rests on the Magnificent-7 remaining magnificent. If they don’t disappoint investors, the S&P 500 likely won’t either given their hefty collective share of the index’s market capitalization. … However, a competitive threat to their magnificence has emerged from China: DeepSeek, with reportedly cheaper AI. Could DeepSeek deep-six the Mag-7? … Check out the accompanying chart collection.

Strategy I: Earnings-Led Bull Market in 2025

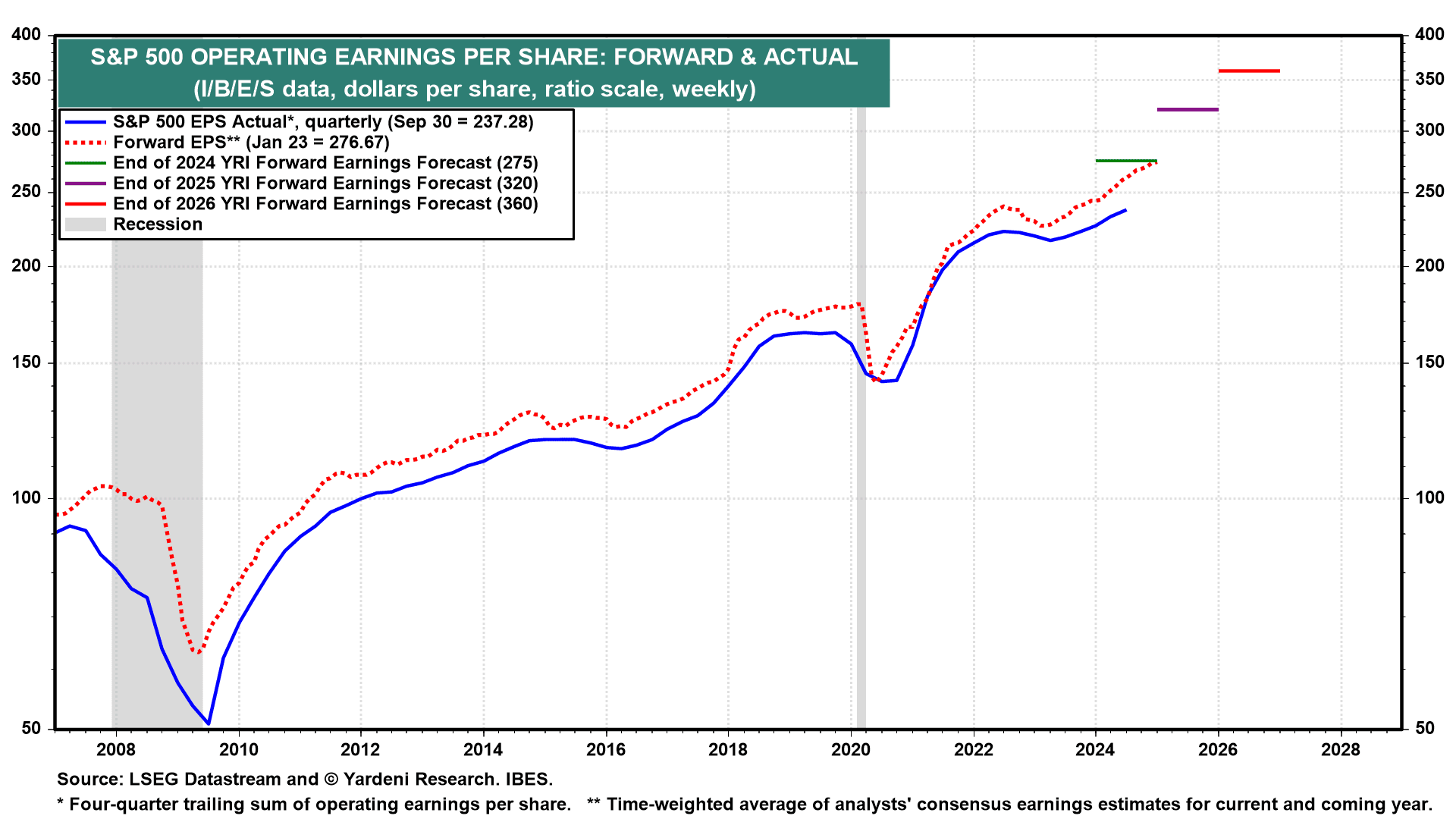

The current bull market in stocks started on October 12, 2022. Since then, the S&P 500 soared 71.1% from a low of 3577.03 to a record high of 6118.71 on Thursday of last week. Over this period, the forward P/E of the S&P 500 stocks as a group rose 46.7% from 15.2 to 22.3, while S&P 500 forward earnings rose 17.1%. So the bull market has been significantly driven by the rising valuation multiple. (FYI: Forward earnings is the time-weighted average of analysts’ consensus operating earnings-per-share estimates for the current year and the following one; the forward P/E is the multiple based on forward earnings.)

Last year was a more balanced one for the stock market; the forward P/E rose 9.8%, while forward earnings rose 12.3%. This year, Eric, Joe, and I expect that most of the bull market’s heavy lifting will be attributable to earnings growth. That’s because the valuation multiple is historically high. It will be in meltup territory if it goes much higher, making the market vulnerable to a meltdown.

To be more specific, we project that the S&P 500 will increase 19.0% this year to 7000. We estimate that S&P 500 earnings will rise 15.6% this year to $285 per share. Of course, at the end of this year, the stock market will be discounting 2026 earnings per share, which we project will be $320. Our 7000 target implies that the forward P/E will be 21.9 at the end of this year, unchanged from its current value.

The latest Bloomberg poll of 22 of the Street’s investment strategists shows an average S&P 500 target of 6600 by year-end with average earnings per share at $266 for the year. The highest estimate for the S&P 500 is 7100 and the lowest is 5500. The highest and lowest earnings estimates are $282 and $227.

Here are some related matters:

(1) Revenues growing solidly

Our earnings-per-share projection is based on S&P 500 revenue gains of 4.0% this year. That’s consistent with the historical average since 1995 of 4.3%. The pushback we get is that even if the US economy continues to grow solidly, the rest of the world’s economies are likely to be weak, as recently projected by the International Monetary Fund (see our January 22 Morning Briefing). Then again, the historical average growth rate of revenues includes three US recessions. Almost no one is expecting a recession in 2025.

Meanwhile, forward revenues per share rose to a record high during the January 16 week, with a solid growth trend despite the current weakness in the world economy outside the US. This series is a great weekly coincident indicator of actual S&P 500 revenues per share.

(2) Profit margin in record-high territory

We are estimating that the S&P 500 profit margin rose to 12.5% in 2024, up from 11.9% in 2023 and below the record high of 13.3% during 2021. We are projecting that the profit margin will rise to a record high of 13.9% this year and 14.9% in 2026. That’s consistent with our productivity-led Roaring 2020s scenario. We are encouraged to see that the S&P 500 forward profit margin rose to a record high of 13.7% during the January 23 week.

We are also expecting that Trump 2.0 will include a cut in the corporate tax rate from 21% to 15% later this year. What about the rise in interest rates? Corporations refinanced much of their long-term debt at record lows during the pandemic. Indeed, the net interest paid by nonfinancial corporations as a percentage of their after-tax profits fell to 7.6% during Q3-2024, the lowest since Q4-1955. This series might start rising in 2025, but not enough to offset the positive impact on the profit margin of higher productivity growth and a lower tax rate, in our opinion.

(3) Coincident economic index bullish for earnings

As noted above, given the economic weakness overseas, we are encouraged to see that S&P 500 forward earnings is on a solid uptrend and at a record high. It continues to track the US Index of Coincident Economic Indicators.

It is interesting to see the recent divergence between the forward earnings of the S&P 500 and that of the S&P 500 Air Freight & Logistics industry. The latter series reflects global economic activity, and it has been falling since early 2022 when the Fed started to tighten monetary policy, Russia launched its invasion of Ukraine (which depressed Europe’s economy), and China’s property market imploded. Yet by early September 2023, the S&P 500 forward earnings was rising to new record highs!

Strategy II: Concentration Update

We are assuming that the forward P/E of the S&P 500 will remain between 21.0 and 22.0 this year, and probably next year too. That’s because we believe that the Magnificent-7 stocks will remain magnificent, maintaining a collective forward P/E around 30.0, while the rest of the stocks in the index, the “S&P 493,” continue to trade collectively around a 20.0 multiple—in other words, the levels they trade at now.

The S&P 500 is likely to remain concentrated. The S&P 500 Information Technology and Communication Services sectors currently account for a record 41.4% of the market capitalization of the S&P 500. They also account for a record 35.1% of the forward earnings of the S&P 500.

The current market cap of both these sectors together is $21.2 trillion. They include five of the Magnificent-7 stocks, all but Amazon and Tesla, which are included in the S&P 500 Consumer Discretionary sector. However, the collective market capitalization of the Magnificent-7 is currently $18.0 trillion.

Strategy III: What Could Possibly Go Wrong?

Might DeepSeek deep-six the Magnificent-7? In last Thursday’s Morning Briefing, Jackie wrote about China’s AI ambitions and observed the following: “The latest startup capturing headlines is DeepSeek. The company shocked the tech industry when it reportedly spent only $5.6 million over two months to develop its latest LLM, which outperformed rival US LLMs from Meta and ChatGPT, a January 21 SCMP article reported. The company kept costs down by using less powerful Nvidia H800 chips. DeepSeek was spun out of High-Flyer Quant, a Chinese quantitative hedge fund. High-Flyer was developing AI to help it research stocks, and both firms are headed by Liang Wenfeng.”

Jackie scooped CNBC, which posted an article on Friday morning titled “How China’s new AI model DeepSeek is threatening U.S. dominance.” The key conclusion for stock investors was the first paragraph: “A little-known AI lab out of China has ignited panic throughout Silicon Valley after releasing AI models that can outperform America’s best despite being built more cheaply and with less-powerful chips.”

Not much is known about DeepSeek. It’s a Chinese company with a website that claims: “DeepSeek-V3 achieves a significant breakthrough in inference speed over previous models. It tops the leaderboard among open-source models and rivals the most advanced closed-source models globally.” The company’s technical report about this LLM is also available online.

One skeptic on LinkedIn views this development as a plot by the Chinese Communist Party to undermine American AI innovation. He observes that the reported costs to train the LLM are suspiciously low. The fact that it is available on an open-source basis suggests that the Chinese aim to be the low-cost producers of AI, reducing the competitiveness of US developed private AI systems.

Jackie also scooped The Wall Street Journal, which posted an excellent article on this subject at 12:00 a.m. Sunday morning titled “Silicon Valley Is Raving About a Made-in-China AI Model DeepSeek.” Marc Andreessen, the Silicon Valley venture capitalist who has been advising President Trump, in an X post on Friday raved: “Deepseek R1 is one of the most amazing and impressive breakthroughs I’ve ever seen—and as open source, a profound gift to the world.”

In our Sunday morning QuickTakes, we concluded the following about the impact of DeepSeek on the Mag-7:

(1) “This might be bad news for the Mag-7 that have plans to dominate the AI market with their (expensive) AI services. On the other hand, it might mean that AI systems will be more accessible and cheaper. If so, the best way to play AI might be the S&P 493 companies that will be cutting their costs and boosting their productivity using this new technology.”

(2) “It might be good news for the Mag-7 that can learn from DeepSeek to design AI systems with cheaper GPUs. That would reduce their capital spending and boost their profits. It might not be a happy development for Nvidia.”

We are even more confident in our technology-driven, productivity-led Roaring 2020s scenario and are sticking with our S&P 500 targets of 7000 for 2025, 8000, for 2026 and 10,000 for 2029.

Strategy IV: Will 2024 Laggards Be the Leaders in 2025?

If it turns out that AI systems can be developed at a much lower cost than suggested by the enormous AI-related capital spending by American AI companies, and especially the Magnificent-7, then these stocks would be vulnerable to a selloff, which would depress the stock market given their weight in the S&P 500. However, such a selloff would be a good opportunity to jump into both the S&P 007 and the S&P 493, which would benefit from the availability of more affordable AI technologies. The S&P 493 have lagged the performance of the Magnificent-7.

We are assuming that US AI companies will achieve what DeepSeek has done as soon as possible; they’ll likely be scrambling to do so. Right now, Elon Musk is busy undercutting Stargate. It is an AI infrastructure joint venture among SoftBank, OpenAI, and Oracle that Trump announced last week on January 21. Their respective companies will invest $100 billion in total for the project to start, with plans to pour up to $500 billion into it in the coming years. Musk questioned whether the venture has the money to back up their ambitions. On Thursday, Trump shrugged off the controversy, saying that Musk “hates one of the people in the deal,” namely Sam Altman of OpenAI.

Perhaps DeepSeek’s accomplishment means that AI systems can be designed much more cheaply than envisioned by Stargate. That would be a positive for everyone.

Executive Summary

The current bull market has been driven mostly by valuation expansion; now valuation is historically high. We expect earnings growth to perpetuate the bull market this year; any more valuation expansion could leave the market vulnerable to a meltdown. Our year-end target for the S&P 500 is 7000, based on a solid rise in earnings with no further valuation expansion. … Much of our optimism rests on the Magnificent-7 remaining magnificent. If they don’t disappoint investors, the S&P 500 likely won’t either given their hefty collective share of the index’s market capitalization. … However, a competitive threat to their magnificence has emerged from China: DeepSeek, with reportedly cheaper AI. Could DeepSeek deep-six the Mag-7? … Check out the accompanying chart collection.

Strategy I: Earnings-Led Bull Market in 2025

The current bull market in stocks started on October 12, 2022. Since then, the S&P 500 soared 71.1% from a low of 3577.03 to a record high of 6118.71 on Thursday of last week. Over this period, the forward P/E of the S&P 500 stocks as a group rose 46.7% from 15.2 to 22.3, while S&P 500 forward earnings rose 17.1%. So the bull market has been significantly driven by the rising valuation multiple. (FYI: Forward earnings is the time-weighted average of analysts’ consensus operating earnings-per-share estimates for the current year and the following one; the forward P/E is the multiple based on forward earnings.)

Last year was a more balanced one for the stock market; the forward P/E rose 9.8%, while forward earnings rose 12.3%. This year, Eric, Joe, and I expect that most of the bull market’s heavy lifting will be attributable to earnings growth. That’s because the valuation multiple is historically high. It will be in meltup territory if it goes much higher, making the market vulnerable to a meltdown.

To be more specific, we project that the S&P 500 will increase 19.0% this year to 7000. We estimate that S&P 500 earnings will rise 15.6% this year to $285 per share. Of course, at the end of this year, the stock market will be discounting 2026 earnings per share, which we project will be $320. Our 7000 target implies that the forward P/E will be 21.9 at the end of this year, unchanged from its current value.

The latest Bloomberg poll of 22 of the Street’s investment strategists shows an average S&P 500 target of 6600 by year-end with average earnings per share at $266 for the year. The highest estimate for the S&P 500 is 7100 and the lowest is 5500. The highest and lowest earnings estimates are $282 and $227.

Here are some related matters:

(1) Revenues growing solidly

Our earnings-per-share projection is based on S&P 500 revenue gains of 4.0% this year. That’s consistent with the historical average since 1995 of 4.3%. The pushback we get is that even if the US economy continues to grow solidly, the rest of the world’s economies are likely to be weak, as recently projected by the International Monetary Fund (see our January 22 Morning Briefing). Then again, the historical average growth rate of revenues includes three US recessions. Almost no one is expecting a recession in 2025.

Meanwhile, forward revenues per share rose to a record high during the January 16 week, with a solid growth trend despite the current weakness in the world economy outside the US. This series is a great weekly coincident indicator of actual S&P 500 revenues per share.

(2) Profit margin in record-high territory

We are estimating that the S&P 500 profit margin rose to 12.5% in 2024, up from 11.9% in 2023 and below the record high of 13.3% during 2021. We are projecting that the profit margin will rise to a record high of 13.9% this year and 14.9% in 2026. That’s consistent with our productivity-led Roaring 2020s scenario. We are encouraged to see that the S&P 500 forward profit margin rose to a record high of 13.7% during the January 23 week.

We are also expecting that Trump 2.0 will include a cut in the corporate tax rate from 21% to 15% later this year. What about the rise in interest rates? Corporations refinanced much of their long-term debt at record lows during the pandemic. Indeed, the net interest paid by nonfinancial corporations as a percentage of their after-tax profits fell to 7.6% during Q3-2024, the lowest since Q4-1955. This series might start rising in 2025, but not enough to offset the positive impact on the profit margin of higher productivity growth and a lower tax rate, in our opinion.

(3) Coincident economic index bullish for earnings

As noted above, given the economic weakness overseas, we are encouraged to see that S&P 500 forward earnings is on a solid uptrend and at a record high. It continues to track the US Index of Coincident Economic Indicators.

It is interesting to see the recent divergence between the forward earnings of the S&P 500 and that of the S&P 500 Air Freight & Logistics industry. The latter series reflects global economic activity, and it has been falling since early 2022 when the Fed started to tighten monetary policy, Russia launched its invasion of Ukraine (which depressed Europe’s economy), and China’s property market imploded. Yet by early September 2023, the S&P 500 forward earnings was rising to new record highs!

Strategy II: Concentration Update

We are assuming that the forward P/E of the S&P 500 will remain between 21.0 and 22.0 this year, and probably next year too. That’s because we believe that the Magnificent-7 stocks will remain magnificent, maintaining a collective forward P/E around 30.0, while the rest of the stocks in the index, the “S&P 493,” continue to trade collectively around a 20.0 multiple—in other words, the levels they trade at now.

The S&P 500 is likely to remain concentrated. The S&P 500 Information Technology and Communication Services sectors currently account for a record 41.4% of the market capitalization of the S&P 500. They also account for a record 35.1% of the forward earnings of the S&P 500.

The current market cap of both these sectors together is $21.2 trillion. They include five of the Magnificent-7 stocks, all but Amazon and Tesla, which are included in the S&P 500 Consumer Discretionary sector. However, the collective market capitalization of the Magnificent-7 is currently $18.0 trillion.

Strategy III: What Could Possibly Go Wrong?

Might DeepSeek deep-six the Magnificent-7? In last Thursday’s Morning Briefing, Jackie wrote about China’s AI ambitions and observed the following: “The latest startup capturing headlines is DeepSeek. The company shocked the tech industry when it reportedly spent only $5.6 million over two months to develop its latest LLM, which outperformed rival US LLMs from Meta and ChatGPT, a January 21 SCMP article reported. The company kept costs down by using less powerful Nvidia H800 chips. DeepSeek was spun out of High-Flyer Quant, a Chinese quantitative hedge fund. High-Flyer was developing AI to help it research stocks, and both firms are headed by Liang Wenfeng.”

Jackie scooped CNBC, which posted an article on Friday morning titled “How China’s new AI model DeepSeek is threatening U.S. dominance.” The key conclusion for stock investors was the first paragraph: “A little-known AI lab out of China has ignited panic throughout Silicon Valley after releasing AI models that can outperform America’s best despite being built more cheaply and with less-powerful chips.”

Not much is known about DeepSeek. It’s a Chinese company with a website that claims: “DeepSeek-V3 achieves a significant breakthrough in inference speed over previous models. It tops the leaderboard among open-source models and rivals the most advanced closed-source models globally.” The company’s technical report about this LLM is also available online.

One skeptic on LinkedIn views this development as a plot by the Chinese Communist Party to undermine American AI innovation. He observes that the reported costs to train the LLM are suspiciously low. The fact that it is available on an open-source basis suggests that the Chinese aim to be the low-cost producers of AI, reducing the competitiveness of US developed private AI systems.

Jackie also scooped The Wall Street Journal, which posted an excellent article on this subject at 12:00 a.m. Sunday morning titled “Silicon Valley Is Raving About a Made-in-China AI Model DeepSeek.” Marc Andreessen, the Silicon Valley venture capitalist who has been advising President Trump, in an X post on Friday raved: “Deepseek R1 is one of the most amazing and impressive breakthroughs I’ve ever seen—and as open source, a profound gift to the world.”

In our Sunday morning QuickTakes, we concluded the following about the impact of DeepSeek on the Mag-7:

(1) “This might be bad news for the Mag-7 that have plans to dominate the AI market with their (expensive) AI services. On the other hand, it might mean that AI systems will be more accessible and cheaper. If so, the best way to play AI might be the S&P 493 companies that will be cutting their costs and boosting their productivity using this new technology.”

(2) “It might be good news for the Mag-7 that can learn from DeepSeek to design AI systems with cheaper GPUs. That would reduce their capital spending and boost their profits. It might not be a happy development for Nvidia.”

We are even more confident in our technology-driven, productivity-led Roaring 2020s scenario and are sticking with our S&P 500 targets of 7000 for 2025, 8000, for 2026 and 10,000 for 2029.

Strategy IV: Will 2024 Laggards Be the Leaders in 2025?

If it turns out that AI systems can be developed at a much lower cost than suggested by the enormous AI-related capital spending by American AI companies, and especially the Magnificent-7, then these stocks would be vulnerable to a selloff, which would depress the stock market given their weight in the S&P 500. However, such a selloff would be a good opportunity to jump into both the S&P 007 and the S&P 493, which would benefit from the availability of more affordable AI technologies. The S&P 493 have lagged the performance of the Magnificent-7.

We are assuming that US AI companies will achieve what DeepSeek has done as soon as possible; they’ll likely be scrambling to do so. Right now, Elon Musk is busy undercutting Stargate. It is an AI infrastructure joint venture among SoftBank, OpenAI, and Oracle that Trump announced last week on January 21. Their respective companies will invest $100 billion in total for the project to start, with plans to pour up to $500 billion into it in the coming years. Musk questioned whether the venture has the money to back up their ambitions. On Thursday, Trump shrugged off the controversy, saying that Musk “hates one of the people in the deal,” namely Sam Altman of OpenAI.

Perhaps DeepSeek’s accomplishment means that AI systems can be designed much more cheaply than envisioned by Stargate. That would be a positive for everyone.

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »