Executive Summary

The Bond Vigilantes aren’t saddling up just yet, but they’re on high alert, Ed reports. They’re watching to see whether anti-DOGE gunslingers will cripple the new federal department or whether DOGE will root out sufficient government inefficiencies to enable Trump 2.0 to slow the budget deficit’s growth and proceed on its tax-cut plans. The stakes are high for the US economy and financial markets, as the Bond Vigilantes have never carried more firepower in their holsters. Fortunately, Treasury Security Bessent is keeping the administration mindful of that. … Also: Eric puts January’s retail sales report in sanguine perspective and discusses industrial production data suggesting a rolling recovery in US manufacturing. … Check out the accompanying chart collection.

Federal Budget I: The DOGE Boys

“The Gunfight at Dodge City” is a 1959 Western film. After his brother the sheriff is murdered, Bat Masterson is elected to the job of sheriff and is determined to find the killer and make Dodge City safe. Today, there are gunfights going on in DOGE City to restore law and order to fiscal policy. Will the new sheriff in town get the job done, or will the Bond Vigilantes do it?

The Department of Government Efficiency (DOGE), led by Elon Musk (who reminds us of a superhero on a mission to save humanity), is scrambling to uncover waste and fraud in the federal government. That should be easy. The question is whether he and his team—a.k.a. the DOGE Boys—can find enough waste and fraud to make a big difference to the federal budget outlook if eliminated.

The reason the boys are scrambling is that the Democrats are regrouping and coming to DOGE City for a gunfight. The Democrats have rounded up a posse of Democratic district attorneys from all around the country to stop Musk’s muckrakers by filing motions in courts to block them from raking the muck they find.

Treasury Secretary Scott Bessent probably also alerted the DOGE Boys that the Bond Vigilantes might be coming to DOGE City for a shootout if the Trump administration doesn’t convince them there’s no need for a gunfight because the President will deliver fiscal discipline and resist telling the Fed to lower interest rates.

After all, the Fed did lower the federal funds rate (FFR) by 100bps from September 18 through December 18 last year, but the Bond Vigilantes immediately expressed their dismay that monetary policy was stimulating an economy that didn’t need to be stimulated and enabling fiscal excesses. They did so by pushing the bond yield higher by 100bps.

▌View Related Live Charts: US - Treasury Yields vs. Fed Funds Rate

▌View Related Live Charts: US - Treasury Yields vs. Fed Funds Rate

In the past, the Fed lowered the FFR from cyclical peaks because the peaks were followed by recessions. There has been no recession this time.

▌View Related Live Charts: US - Federal Fund Interest Rates

▌View Related Live Charts: US - Federal Fund Interest Rates

Now, consider a few of the recent developments that led up to the trouble brewing in DOGE City:

(1) Summer 2024 Elon Musk floated the concept of DOGE in discussions with Donald Trump during the summer of 2024 as the then-former President campaigned for a second term. In an August campaign event, Trump said that, if elected, he would consider giving Musk an advisory role on how to streamline the government. Musk immediately tweeted, “I am willing to serve.”

(2) October 27, 2024

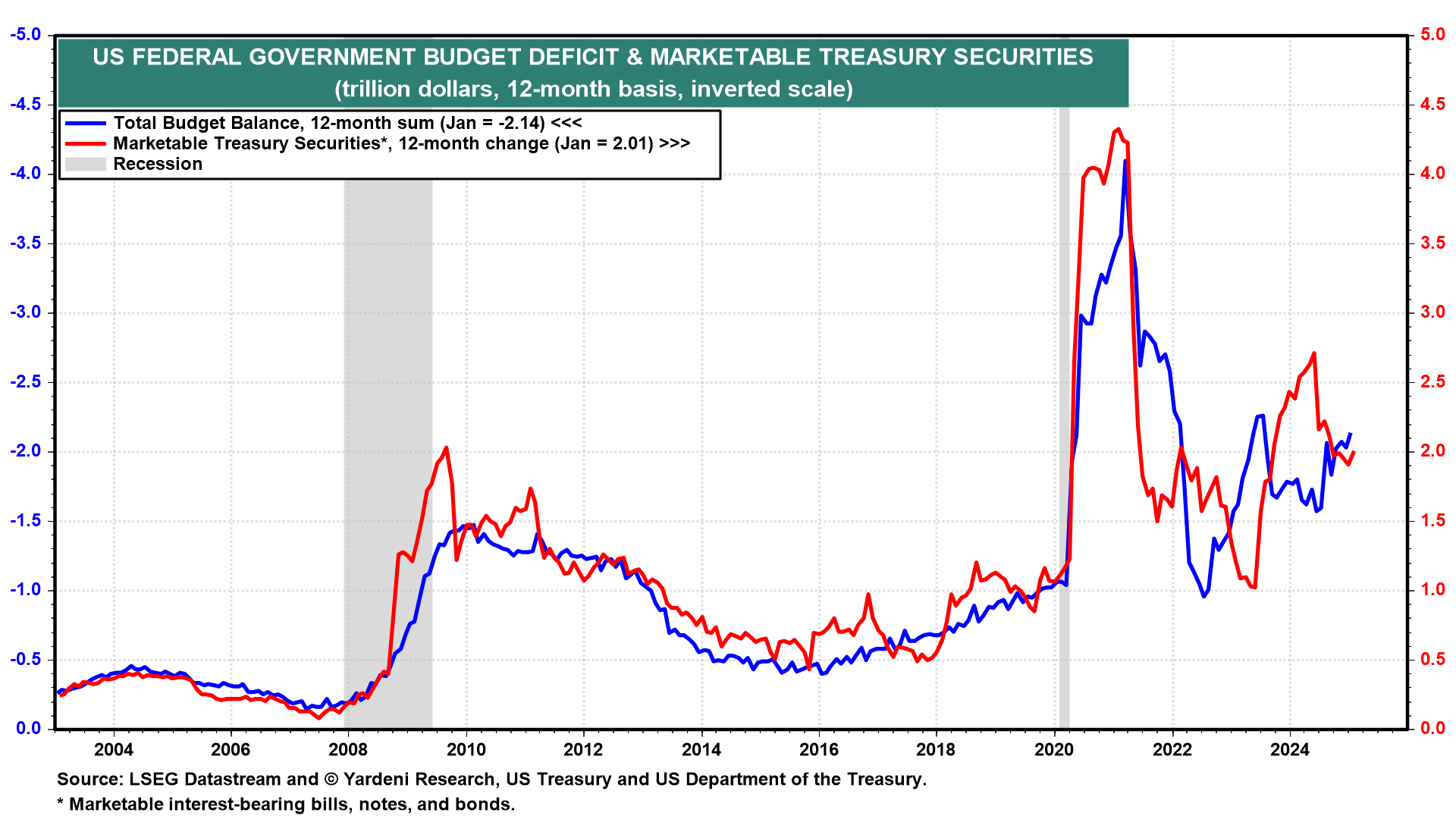

Elon Musk first declared that DOGE would cut $2 trillion from the federal budget on October 27, 2024, during a Trump rally at Madison Square Garden. Over the 12 months through January, the federal government’s budget deficit totaled $2.14 trillion.

▌View Related Live Charts: US - Federal Surplus Or Deficit (Monthly)

▌View Related Live Charts: US - Federal Surplus Or Deficit (Monthly)

(3) January 8, 2024

However, on January 8, 2025, Musk stated in an interview with Mark Penn that achieving the $2 trillion cut was unlikely and that the best-case outcome would be around $1 trillion. Over the past 12 months through January, federal government outlays totaled $7.1 trillion, with $6.0 trillion in mandatory outlays (including Social Security, Medicare, health, income security, national defense, and net interest). Net interest outlays alone totaled $920.6 billion, exceeding the $910.2 billion spent on defense over the last 12 months.

▌View Related Live Charts: US - Federal Outlays (Monthly)

▌View Related Live Charts: US - Federal Outlays (Monthly)

(4) January 20, 2025 On Inauguration Day, President Trump signed an Executive Order titled “Establishing and Implementing the President’s ‘Department of Government Efficiency.’” The order renamed the existing United States Digital Service “the United States DOGE Service” (USDS). Within the USDS, a new organization was established, the US DOGE Service Temporary Organization, which is headed by the USDS administrator (Musk) and is scheduled to be terminated on July 4, 2026.

Each government agency must establish a “DOGE Team of at least four employees, which may include Special Government Employees, hired or assigned within thirty days of the date of this Order. Agency Heads shall select the DOGE Team members in consultation with the USDS Administrator. Each DOGE Team will typically include one DOGE Team Lead, one engineer, one human resources specialist, and one attorney.”

The goal of this Executive Order is to modernize “federal technology and software to maximize efficiency and productivity.” To achieve that, the DOGE Teams will have “full and prompt access to all unclassified agency records, software systems, and IT systems.”

Needless to say, DOGE has stirred up lots of controversy in Washington. There are almost daily headlines on DOGE’s success at finding lots of inefficiencies, waste, and possible fraud within the government accounts. Many of these headlines are generated by Musk’s tweets on X.

There is lots of pushback by Democrats, who are challenging the legality of the DOGE Boys’ flipping through government files. Douglas Holtz-Eakin, who had served as the director of the Congressional Budget Office, compared DOGE to the former Grace Commission, which had zero of its 150 proposals enacted.

Federal Budget II: In Bessent We Trust

It’s too soon to tell how much DOGE will reduce government spending. However, Treasury Secretary Bessent is certainly aware of the need to reduce the federal budget deficit relative to nominal GDP. He has committed to halving this ratio from 6% to 3%.

This ratio was last at 3% during Q4-2015 (2.93%, to be exact). Since then, Trump 1.0 tax cuts drove it up to 4.65% during Q4-2019 (just before the pandemic), and Biden’s outlays raised it over 6% during Q4-2024.

Trump 2.0 is borrowing a page from the Clinton administration’s playbook, specifically the one in which Robert Rubin and James Carville warned Clinton that he had to respect the power of the Bond Vigilantes and maintain fiscal discipline. On February 6, US Treasury Secretary Scott Bessent said that he and President Trump are less concerned about the federal funds rate (FFR) and instead are hoping to contain the 10-year Treasury yield. Bessent’s message to the Bond Vigilantes was that he has explained to President Trump that they have the power to stymie his fiscal agenda.

However, on February 12, Trump posted the following on his Truth Social platform: “Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!!” That assertion flew in the face of economists’ expectations that tariffs would fuel inflation and postpone rate cuts as well as what Federal Reserve Chair Jerome Powell told US lawmakers the day before: that the Fed was in no rush to cut its short-term interest rate again given an economy that is strong overall.

The Bond Vigilantes are biding their time, waiting to see how much the Trump administration can slow the increase in federal spending because of the efforts of the DOGE Boys. If they don’t deliver enough spending cuts, there could be a gunfight at DOGE City, with the Bond Vigilantes shooting holes in the Trump administration’s fiscal agenda, including the extension of his tax cuts.

It is good that Bessent understands the power of the Bond Vigilantes. In effect, he represents their interests within the Trump administration. Eric and I believe that by appointing Bessent as Treasury Secretary and establishing DOGE, Trump bought his administration some time to deal with the federal budget mess.

Federal Budget III: Tracking The Bond Vigilantes

“Bond Vigilantes” is the phrase I coined in July 1983 to refer to bond investors, acting in their own financial interests, when their activity drives up bond yields out of belief that the government will fail in its duty to keep the budget deficit from ballooning and inflation contained via fiscal and monetary policy. They’ll demand greater yield for their long-term bond investments if they think the value of their investment will be eroded by inflation over the term. Higher bond market yields effectively push up other interest rates—so it’s as if bond investors are taking fiscal and monetary discipline into their own hands, vigilante style, when the government drops the ball. (See The Bond Vigilantes excerpt from my 2018 book Predicting the Markets.)

One way to monitor the activities of the Bond Vigilantes is to compare the 10-year Treasury bond yield to the growth in nominal GDP on a y/y basis. When the spread is positive while the economy is growing, they are doing what they can to slow it down. They were asleep at the reins during the 1960s and 1970s, when inflation got out of hand. They were much more vigilant during the 1980s and early 1990s.

▌View Related Live Charts: US - 10-Year Treasury Yield, US - Nominal GDP (% of Global Nominal GDP)

▌View Related Live Charts: US - 10-Year Treasury Yield, US - Nominal GDP (% of Global Nominal GDP)

The Bond Vigilantes were stymied by the Fed’s QE (quantitative easing, i.e., buying bonds) and ZIRP (i.e., zero-interest-rate policy) from 2008 through 2022, i.e., between the Great Financial Crisis and the Great Virus Crisis, when the Fed’s monetary stance was ultra easy. The bond market was rigged by the Fed during this period. The Fed tightened monetary policy by raising the FFR and ending QE from March 2022 through August 2024, allowing the bond yield to normalize.

The 10-year Treasury bond yield is currently about 4.50%, having risen back up to around where it was before the Great Financial Crisis (Fig. 9). The spread between the bond yield and the growth rate in nominal GDP was -70bps during Q4-2024. It remains around zero currently. Nominal GDP growth was 5.0% y/y during Q4.

We conclude that the Bond Vigilantes aren’t saddling up just yet to ride into DOGE City for a gunfight with the Trump administration. But ask us again if the yield jumps above 5.0% with attendant widespread fear that it is heading toward 6.0%.

The Bond Vigilantes have never been potentially more powerful than right now given that total federal public debt outstanding is a record $36.2 trillion with a record $28.5 trillion in marketable US Treasury securities.

▌View Related Live Charts: US - Total Public Debt Outstanding

▌View Related Live Charts: US - Total Public Debt Outstanding

Economy I: Seasonal Sales Issues

Retail sales fell 0.9% m/m in January, one of the worst monthly readings in years. And because of the 0.7% m/m increase in CPI goods inflation, real retail sales fell by 1.6% m/m last month. Those are ugly numbers, and they brought a few bears out of hibernation to proclaim that the long-awaited economic slowdown is here!

▌View Related Live Charts: US - Consumer Price Index - Core Goods

▌View Related Live Charts: US - Consumer Price Index - Core Goods

We’re not too worried about January’s one-off dip in spending; January is always a bad month for retail sales after December’s spending bonanza and before seasonal adjustment. We continue to be optimistic on the US consumer. Here’s more:

(1) Smoothing out seasonals

The Census Bureau’s seasonal adjustment is an attempt to smooth out the December surge and January plummet in spending each year. For instance, retail sales fell 16.5% m/m in January on a non-seasonally adjusted basis, a tad less than it fell in January 2024 (-16.8%) and 2022 (-17.0%) and a bit more than it fell in 2023 (-14.8%).

In several economic indicators, including retail sales, the seasonal adjustments haven’t fully caught up to the post-pandemic shifts in consumer behavior. January's retail sales rose 4.2% y/y on a seasonally adjusted basis and 4.8% not seasonally adjusted.

The Redbook retail sales series shows a solid increase of 5.3% y/y through the week of February 7, 2024 in nominal terms. It has a good correlation with the comparable growth rate for monthly retail sales excluding food services. We also note that the winter deep freeze, and perhaps the fires in California, likely weighed on consumer activity last month.

▌View Related Live Charts: US - Redbook Same Store Retail Sales Index (YoY)

▌View Related Live Charts: US - Redbook Same Store Retail Sales Index (YoY)

▌View Related Live Charts: US - Employment Level - With A Job, Not at Work, Bad Weather

▌View Related Live Charts: US - Employment Level - With A Job, Not at Work, Bad Weather

(2) Auto regression

After a very strong Q4, auto sales fell off in January. The seasonally adjusted annualized rate for total new-vehicle sales fell from 16.9 million units in December to 15.6 million in January. We believe auto dealers used discounts to clear out their inventories heading into the end of last year, which contributed to the big drop in Q4-2024 GDP inventory investment but also spurred a lot of sales. So in Q1, we're likely to see inventories rebuilt but sales slow a little.

▌View Related Live Charts: US - Total Vehicle Sales (SAAR), US - Light Weight Vehicle Sales - Autos and Light Trucks (SAAR)

▌View Related Live Charts: US - Total Vehicle Sales (SAAR), US - Light Weight Vehicle Sales - Autos and Light Trucks (SAAR)

Auto sales (-2.8% m/m) was the biggest overall drag on January retail sales. Sporting goods, hobby & bookstores (-4.6%) experienced the largest monthly drop off. We expect that the category also suffered from some seasonal adjustment misreads and will likely rebound next month.

Economy II: Manufacturing Mojo

Hours worked by manufacturing employees fell by 0.7% m/m in January, which typically would suggest that industrial production fell by about the same amount. However, industrial production rose 0.5% m/m after adding 1.0% in December. We had expected the bad weather to weigh unduly on hours worked, but we thought it would be less likely to influence manufacturing. So the increase was encouraging and suggests US manufacturing may be in the first inning of its rolling recovery. The 2.0% y/y increase in production is the largest increase since the Fed began its last round of rate hikes in 2022.

▌View Related Live Charts: US - Industrial Production Index

▌View Related Live Charts: US - Industrial Production Index

Looking deeper at the latest industrial production data, the restarting of Boeing’s production after worker strikes accounted for 0.2ppts of the total 0.5% increase, according to the Fed. Aerospace rose 6.0% m/m, while the index for utilities jumped 7.2% due to demand for heating. Utilities production continues to make new monthly highs, and the demand for data processing and new energy sources from the AI boom suggest it won’t be stopping.

Autos fell 5.2% m/m, dragging on the index for manufacturing output. Given Trump 2.0 initiatives to reshore auto manufacturing, we think OEMs have enough stick and carrot to pick up production by the end of the quarter.

Dr. Yardeni’s 2025 Outlook: AI, Tariffs & Power Plays – The Battle for Economic Dominance Early access is now open for MM Prime! Don’t miss this opportunity to stay ahead of market trends and seize your advantage!

Executive Summary

The Bond Vigilantes aren’t saddling up just yet, but they’re on high alert, Ed reports. They’re watching to see whether anti-DOGE gunslingers will cripple the new federal department or whether DOGE will root out sufficient government inefficiencies to enable Trump 2.0 to slow the budget deficit’s growth and proceed on its tax-cut plans. The stakes are high for the US economy and financial markets, as the Bond Vigilantes have never carried more firepower in their holsters. Fortunately, Treasury Security Bessent is keeping the administration mindful of that. … Also: Eric puts January’s retail sales report in sanguine perspective and discusses industrial production data suggesting a rolling recovery in US manufacturing. … Check out the accompanying chart collection.

Federal Budget I: The DOGE Boys

“The Gunfight at Dodge City” is a 1959 Western film. After his brother the sheriff is murdered, Bat Masterson is elected to the job of sheriff and is determined to find the killer and make Dodge City safe. Today, there are gunfights going on in DOGE City to restore law and order to fiscal policy. Will the new sheriff in town get the job done, or will the Bond Vigilantes do it?

The Department of Government Efficiency (DOGE), led by Elon Musk (who reminds us of a superhero on a mission to save humanity), is scrambling to uncover waste and fraud in the federal government. That should be easy. The question is whether he and his team—a.k.a. the DOGE Boys—can find enough waste and fraud to make a big difference to the federal budget outlook if eliminated.

The reason the boys are scrambling is that the Democrats are regrouping and coming to DOGE City for a gunfight. The Democrats have rounded up a posse of Democratic district attorneys from all around the country to stop Musk’s muckrakers by filing motions in courts to block them from raking the muck they find.

Treasury Secretary Scott Bessent probably also alerted the DOGE Boys that the Bond Vigilantes might be coming to DOGE City for a shootout if the Trump administration doesn’t convince them there’s no need for a gunfight because the President will deliver fiscal discipline and resist telling the Fed to lower interest rates.

After all, the Fed did lower the federal funds rate (FFR) by 100bps from September 18 through December 18 last year, but the Bond Vigilantes immediately expressed their dismay that monetary policy was stimulating an economy that didn’t need to be stimulated and enabling fiscal excesses. They did so by pushing the bond yield higher by 100bps.

▌View Related Live Charts: US - Treasury Yields vs. Fed Funds Rate

In the past, the Fed lowered the FFR from cyclical peaks because the peaks were followed by recessions. There has been no recession this time.

▌View Related Live Charts: US - Federal Fund Interest Rates

Now, consider a few of the recent developments that led up to the trouble brewing in DOGE City:

(1) Summer 2024 Elon Musk floated the concept of DOGE in discussions with Donald Trump during the summer of 2024 as the then-former President campaigned for a second term. In an August campaign event, Trump said that, if elected, he would consider giving Musk an advisory role on how to streamline the government. Musk immediately tweeted, “I am willing to serve.”

(2) October 27, 2024

Elon Musk first declared that DOGE would cut $2 trillion from the federal budget on October 27, 2024, during a Trump rally at Madison Square Garden. Over the 12 months through January, the federal government’s budget deficit totaled $2.14 trillion.

▌View Related Live Charts: US - Federal Surplus Or Deficit (Monthly)

(3) January 8, 2024

However, on January 8, 2025, Musk stated in an interview with Mark Penn that achieving the $2 trillion cut was unlikely and that the best-case outcome would be around $1 trillion. Over the past 12 months through January, federal government outlays totaled $7.1 trillion, with $6.0 trillion in mandatory outlays (including Social Security, Medicare, health, income security, national defense, and net interest). Net interest outlays alone totaled $920.6 billion, exceeding the $910.2 billion spent on defense over the last 12 months.

▌View Related Live Charts: US - Federal Outlays (Monthly)

(4) January 20, 2025 On Inauguration Day, President Trump signed an Executive Order titled “Establishing and Implementing the President’s ‘Department of Government Efficiency.’” The order renamed the existing United States Digital Service “the United States DOGE Service” (USDS). Within the USDS, a new organization was established, the US DOGE Service Temporary Organization, which is headed by the USDS administrator (Musk) and is scheduled to be terminated on July 4, 2026.

Each government agency must establish a “DOGE Team of at least four employees, which may include Special Government Employees, hired or assigned within thirty days of the date of this Order. Agency Heads shall select the DOGE Team members in consultation with the USDS Administrator. Each DOGE Team will typically include one DOGE Team Lead, one engineer, one human resources specialist, and one attorney.”

The goal of this Executive Order is to modernize “federal technology and software to maximize efficiency and productivity.” To achieve that, the DOGE Teams will have “full and prompt access to all unclassified agency records, software systems, and IT systems.”

Needless to say, DOGE has stirred up lots of controversy in Washington. There are almost daily headlines on DOGE’s success at finding lots of inefficiencies, waste, and possible fraud within the government accounts. Many of these headlines are generated by Musk’s tweets on X.

There is lots of pushback by Democrats, who are challenging the legality of the DOGE Boys’ flipping through government files. Douglas Holtz-Eakin, who had served as the director of the Congressional Budget Office, compared DOGE to the former Grace Commission, which had zero of its 150 proposals enacted.

Federal Budget II: In Bessent We Trust

It’s too soon to tell how much DOGE will reduce government spending. However, Treasury Secretary Bessent is certainly aware of the need to reduce the federal budget deficit relative to nominal GDP. He has committed to halving this ratio from 6% to 3%.

This ratio was last at 3% during Q4-2015 (2.93%, to be exact). Since then, Trump 1.0 tax cuts drove it up to 4.65% during Q4-2019 (just before the pandemic), and Biden’s outlays raised it over 6% during Q4-2024.

Trump 2.0 is borrowing a page from the Clinton administration’s playbook, specifically the one in which Robert Rubin and James Carville warned Clinton that he had to respect the power of the Bond Vigilantes and maintain fiscal discipline. On February 6, US Treasury Secretary Scott Bessent said that he and President Trump are less concerned about the federal funds rate (FFR) and instead are hoping to contain the 10-year Treasury yield. Bessent’s message to the Bond Vigilantes was that he has explained to President Trump that they have the power to stymie his fiscal agenda.

However, on February 12, Trump posted the following on his Truth Social platform: “Interest Rates should be lowered, something which would go hand in hand with upcoming Tariffs!!!” That assertion flew in the face of economists’ expectations that tariffs would fuel inflation and postpone rate cuts as well as what Federal Reserve Chair Jerome Powell told US lawmakers the day before: that the Fed was in no rush to cut its short-term interest rate again given an economy that is strong overall.

The Bond Vigilantes are biding their time, waiting to see how much the Trump administration can slow the increase in federal spending because of the efforts of the DOGE Boys. If they don’t deliver enough spending cuts, there could be a gunfight at DOGE City, with the Bond Vigilantes shooting holes in the Trump administration’s fiscal agenda, including the extension of his tax cuts.

It is good that Bessent understands the power of the Bond Vigilantes. In effect, he represents their interests within the Trump administration. Eric and I believe that by appointing Bessent as Treasury Secretary and establishing DOGE, Trump bought his administration some time to deal with the federal budget mess.

Federal Budget III: Tracking The Bond Vigilantes

“Bond Vigilantes” is the phrase I coined in July 1983 to refer to bond investors, acting in their own financial interests, when their activity drives up bond yields out of belief that the government will fail in its duty to keep the budget deficit from ballooning and inflation contained via fiscal and monetary policy. They’ll demand greater yield for their long-term bond investments if they think the value of their investment will be eroded by inflation over the term. Higher bond market yields effectively push up other interest rates—so it’s as if bond investors are taking fiscal and monetary discipline into their own hands, vigilante style, when the government drops the ball. (See The Bond Vigilantes excerpt from my 2018 book Predicting the Markets.)

One way to monitor the activities of the Bond Vigilantes is to compare the 10-year Treasury bond yield to the growth in nominal GDP on a y/y basis. When the spread is positive while the economy is growing, they are doing what they can to slow it down. They were asleep at the reins during the 1960s and 1970s, when inflation got out of hand. They were much more vigilant during the 1980s and early 1990s.

▌View Related Live Charts: US - 10-Year Treasury Yield, US - Nominal GDP (% of Global Nominal GDP)

The Bond Vigilantes were stymied by the Fed’s QE (quantitative easing, i.e., buying bonds) and ZIRP (i.e., zero-interest-rate policy) from 2008 through 2022, i.e., between the Great Financial Crisis and the Great Virus Crisis, when the Fed’s monetary stance was ultra easy. The bond market was rigged by the Fed during this period. The Fed tightened monetary policy by raising the FFR and ending QE from March 2022 through August 2024, allowing the bond yield to normalize.

The 10-year Treasury bond yield is currently about 4.50%, having risen back up to around where it was before the Great Financial Crisis (Fig. 9). The spread between the bond yield and the growth rate in nominal GDP was -70bps during Q4-2024. It remains around zero currently. Nominal GDP growth was 5.0% y/y during Q4.

We conclude that the Bond Vigilantes aren’t saddling up just yet to ride into DOGE City for a gunfight with the Trump administration. But ask us again if the yield jumps above 5.0% with attendant widespread fear that it is heading toward 6.0%.

The Bond Vigilantes have never been potentially more powerful than right now given that total federal public debt outstanding is a record $36.2 trillion with a record $28.5 trillion in marketable US Treasury securities.

▌View Related Live Charts: US - Total Public Debt Outstanding

Economy I: Seasonal Sales Issues

Retail sales fell 0.9% m/m in January, one of the worst monthly readings in years. And because of the 0.7% m/m increase in CPI goods inflation, real retail sales fell by 1.6% m/m last month. Those are ugly numbers, and they brought a few bears out of hibernation to proclaim that the long-awaited economic slowdown is here!

▌View Related Live Charts: US - Consumer Price Index - Core Goods

We’re not too worried about January’s one-off dip in spending; January is always a bad month for retail sales after December’s spending bonanza and before seasonal adjustment. We continue to be optimistic on the US consumer. Here’s more:

(1) Smoothing out seasonals

The Census Bureau’s seasonal adjustment is an attempt to smooth out the December surge and January plummet in spending each year. For instance, retail sales fell 16.5% m/m in January on a non-seasonally adjusted basis, a tad less than it fell in January 2024 (-16.8%) and 2022 (-17.0%) and a bit more than it fell in 2023 (-14.8%).

In several economic indicators, including retail sales, the seasonal adjustments haven’t fully caught up to the post-pandemic shifts in consumer behavior. January's retail sales rose 4.2% y/y on a seasonally adjusted basis and 4.8% not seasonally adjusted.

The Redbook retail sales series shows a solid increase of 5.3% y/y through the week of February 7, 2024 in nominal terms. It has a good correlation with the comparable growth rate for monthly retail sales excluding food services. We also note that the winter deep freeze, and perhaps the fires in California, likely weighed on consumer activity last month.

▌View Related Live Charts: US - Redbook Same Store Retail Sales Index (YoY)

▌View Related Live Charts: US - Employment Level - With A Job, Not at Work, Bad Weather

(2) Auto regression

After a very strong Q4, auto sales fell off in January. The seasonally adjusted annualized rate for total new-vehicle sales fell from 16.9 million units in December to 15.6 million in January. We believe auto dealers used discounts to clear out their inventories heading into the end of last year, which contributed to the big drop in Q4-2024 GDP inventory investment but also spurred a lot of sales. So in Q1, we're likely to see inventories rebuilt but sales slow a little.

▌View Related Live Charts: US - Total Vehicle Sales (SAAR), US - Light Weight Vehicle Sales - Autos and Light Trucks (SAAR)

Auto sales (-2.8% m/m) was the biggest overall drag on January retail sales. Sporting goods, hobby & bookstores (-4.6%) experienced the largest monthly drop off. We expect that the category also suffered from some seasonal adjustment misreads and will likely rebound next month.

Economy II: Manufacturing Mojo

Hours worked by manufacturing employees fell by 0.7% m/m in January, which typically would suggest that industrial production fell by about the same amount. However, industrial production rose 0.5% m/m after adding 1.0% in December. We had expected the bad weather to weigh unduly on hours worked, but we thought it would be less likely to influence manufacturing. So the increase was encouraging and suggests US manufacturing may be in the first inning of its rolling recovery. The 2.0% y/y increase in production is the largest increase since the Fed began its last round of rate hikes in 2022.

▌View Related Live Charts: US - Industrial Production Index

Looking deeper at the latest industrial production data, the restarting of Boeing’s production after worker strikes accounted for 0.2ppts of the total 0.5% increase, according to the Fed. Aerospace rose 6.0% m/m, while the index for utilities jumped 7.2% due to demand for heating. Utilities production continues to make new monthly highs, and the demand for data processing and new energy sources from the AI boom suggest it won’t be stopping.

Autos fell 5.2% m/m, dragging on the index for manufacturing output. Given Trump 2.0 initiatives to reshore auto manufacturing, we think OEMs have enough stick and carrot to pick up production by the end of the quarter.

Dr. Yardeni’s 2025 Outlook: AI, Tariffs & Power Plays – The Battle for Economic Dominance Early access is now open for MM Prime! Don’t miss this opportunity to stay ahead of market trends and seize your advantage!

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »