Dear all,

Global stock markets largely held steady over the past few weeks, with the exception of tech stocks, which faced a pullback triggered by DeepSeek (particularly impacted was the Philadelphia Semiconductor Index, which fell by 8.3%). Overall, January was a positive month for equities, with most indices posting gains: the S&P 500, Dow Jones, European stock indices, and the Taiwanese stock market all registered impressive gains of over 2~9%. Despite volatility during the Lunar New Year break, the Philadelphia Semiconductor Index and Nasdaq still managed to close the month with gains of +0.7% and +1.6%, respectively. In other asset classes, the U.S. dollar and Treasury yields ended the month flat. Oil prices remained relatively weak, with WTI crude consolidating around $73 per barrel, while gold reached an all-time high, breaking above $2,830 per ounce.

Based on the recent releases of key economic data and policies under Trump 2.0, we summarize trends in four key aspects and our thoughts below:

1. Economic Fundamentals: Data Confirms Moderate Growth, Good for Sustaining Market Momentum

On January 30, the U.S. Commerce Department reported that U.S. GDP grew at an annualized rate of 2.3% in Q4 2024 (down from 3.1% in the previous quarter). Although GDP growth slowed, the GDP report actually underscores the health of the U.S. economy. Firstly, consumer spending expanded at a robust pace of 4.2%. Also, changes in inventories recorded a negative contribution of -0.93 percentage points to change in real GDP (suggesting inventories have been depleting). Therefore, although headline GDP growth was down from the previous quarter, a closer look at the details points to the strength of the economy reflected in diminishing inventories.

Strong GDP performance from the U.S., combined with encouraging data from other economies released recently—such as the Eurozone’s Q4 2024 GDP growth of 0.9% (same as the previous quarter), Japan’s solid growth of 3.7% in retail sales in December (prev. 2.8%), and Taiwan’s Q4 2024 GDP growth of 1.84% (down from 4.17% in the previous quarter, mainly due to the surge in imports by 18% and thus not a cause of concern)—suggests a positive global economic backdrop. Overall, economies across the world delivered solid performance in January, suggesting global economic fundamentals remain supportive, with little risk of weighing on stock market performance.

2. Liquidity Environment: Fed Holds Rates as Expected, While ECB and Bank of Canada Continue Easing

On January 29 and 30, the Bank of Canada and the European Central Bank (ECB) each lowered interest rates by 25 basis points. Meanwhile, on January 30, at the Fed’s first policy meeting this year, all committee members voted unanimously to keep the benchmark interest rate steady at 4.25~4.50%. In the FOMC statement, the previous language that the unemployment rate had “moved up” was removed and replaced with “unemployment rate has stabilized at a low level in recent months.” Also, the line about progress made on inflation was removed altogether, with the Fed now describing inflation as remaining “somewhat elevated.” During the post-meeting press conference, Fed chairman Powell stated that, with policy being significantly less restrictive than before and the economy remaining strong, there is no hurry to adjust policy stance at this time.

The meeting outcome aligns with our previous expectations—given stable economic growth, there’s no need for the Fed to rush into any immediate action at the moment. Meanwhile, released on January 31, core PCE inflation eased slightly to 2.79% in December (prev. 2.82%). Given the high base effect in the first half of the year, we anticipate continued easing in inflation, which will help ensure a favorable liquidity environment.

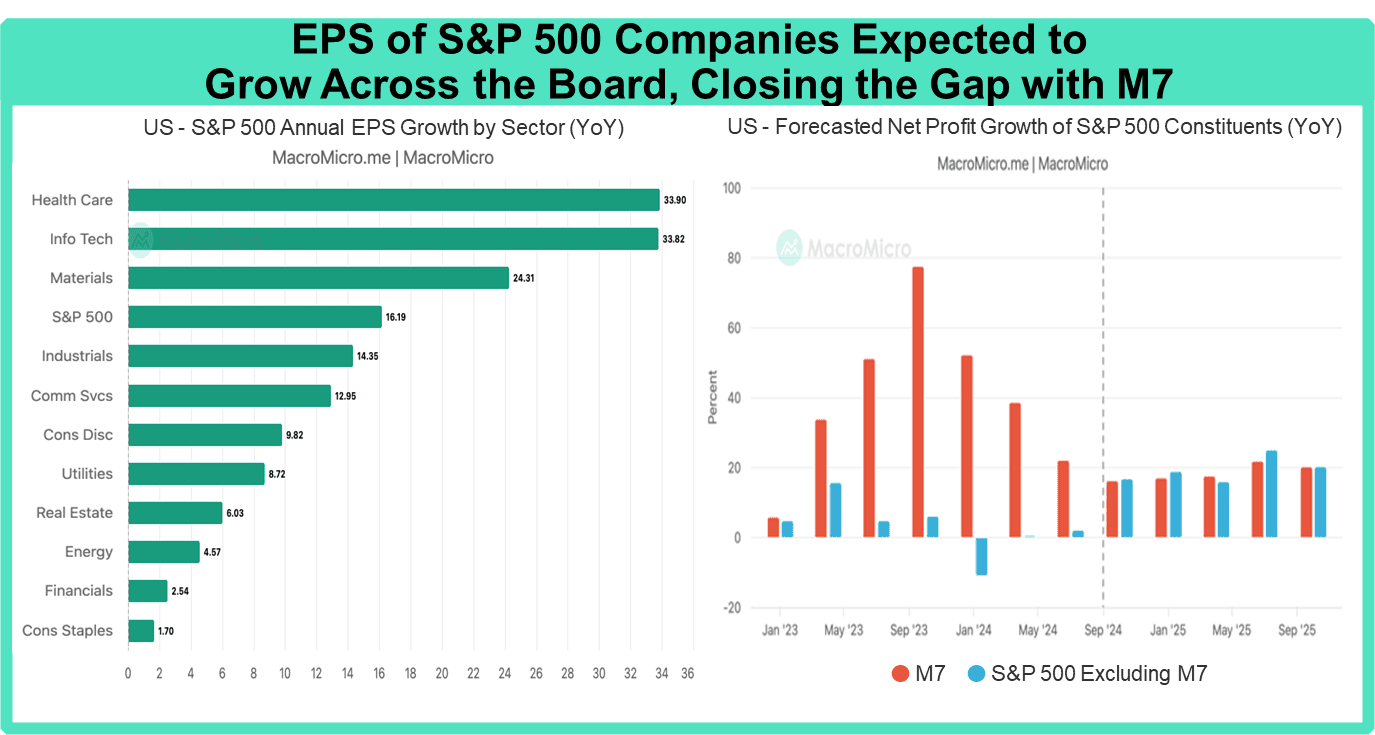

3. Corporate Earnings: 77% of US Companies Beat Forecasts, S&P 500 EPS Expected to Grow by Double Digits This Year

As of the end of January, more than 35% of S&P 500 companies have reported their Q4 2024 earnings, with approximately 77% beating market expectations. According to S&P Global, the estimated year-on-year EPS growth for the S&P 500 is +13.5% in Q4 2024 (prev. 13.2%). In addition to reaching a new record high in earnings, this also marks the first time since 2021 that Q4 EPS has achieved double-digit growth. Furthermore, overall S&P 500 earnings are forecasted to grow at a double-digit 16.19% in 2025, outpacing the 9.26% growth in 2024!

So far, there have been no big surprises from the earnings season in the U.S., while the recent DeepSeek developments served as a reminder of the transformative impact of the productivity cycle. As I mentioned in our 2025 Outlook Report, the next phase of AI development hinges on two pending breakthroughs: advancements in hardware-software integration and reduction of costs. If barriers to AI adoption can be lowered through reduced costs, it could stimulate expansion across more use cases and spur demand for hardware upgrades. The broadening out of competitive advantages from major players holding key resources is also happening faster than we imagined, a trend that will likely be reflected in this year’s earnings reports, transitioning from benefiting only a few leading tech firms to a more widespread uplift. Based on our estimates, net profit growth of the Magnificent Seven (M7) is expected to remain strong at 16~22% from Q4 2024 through Q4 2025. That said, it’s worth noting that the other 493 companies in the S&P 500, whose profit growth had significantly lagged the M7 over the past 6 quarters, are poised to narrow that gap in 2025. All 11 GICS sectors are also projected to see positive EPS growth in 2025 (compared to just 9 sectors in 2024).

4. US Policy Landscape: Trump's Policies in Line with Expectations, No Major Surprises

Upon his inauguration on January 20, Trump signed a total of 26 executive orders, including strict measures to curb illegal immigration and measures to expand traditional energy production. The president also revoked 78 executive orders from the Biden era, swiftly implementing his campaign promises. On tariffs, Trump signed an executive order on February 1, imposing a 25% tariff on goods imported from Canada and Mexico, and a 10% tariff on goods from China starting February 4, primarily aimed at tackling issues like fentanyl smuggling and illegal immigration.

Already a subscriber? Click here to log in.

Full Access to Our Services

Comprehensive data at your service

with key indicators for investment insights

Exclusive flash reports

on key events and data

Create your own charts and analysis

including performance backtesting

Hub of professionals to engage

in meaningful discussions and insights

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »