NVIDIA has once again captured market attention with its fiscal Q1 2025 earnings report, delivering another strong quarter that reinforced its position as the AI industry leader. Despite some margin pressures from product transitions and export restrictions, the company continues to demonstrate robust demand fundamentals, offering crucial signals about the sustainability of the ongoing AI boom. Here’s a breakdown of five key areas for investors to watch:

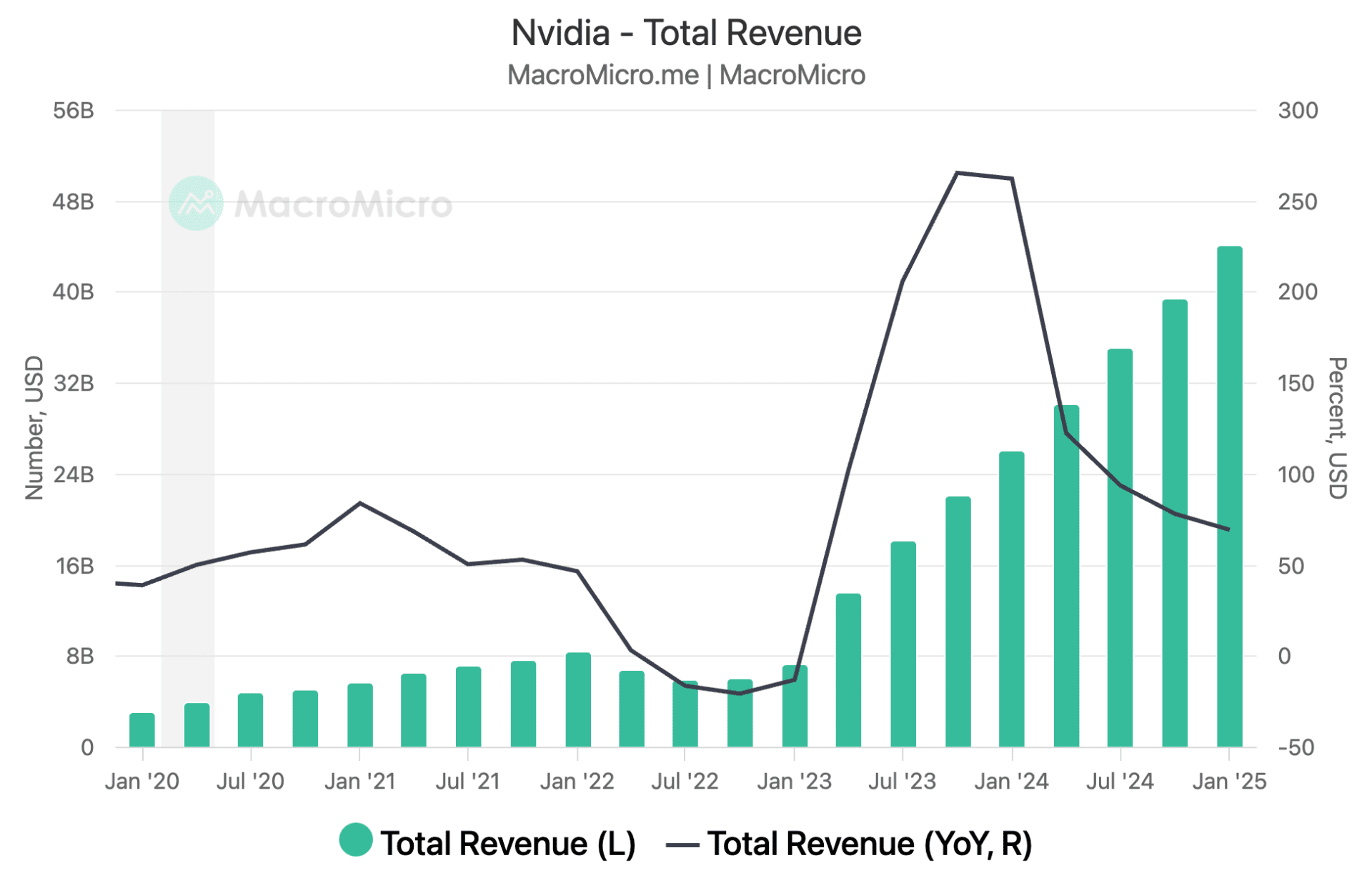

1. Revenue Outlook

NVIDIA delivered solid Q1 2025 performance, though with some notable margin impacts:

- Revenue: $44.06 billion, up 69% YoY (vs. 78% in previous quarter), beating the $43.3 billion consensus.

- Gross Margin: Declined to 60.5% (from previous 73%), reflecting pressures from one-time impairment losses related to H20.

- Operating Margin: 49.1%, down from 61.1%.

- Non-GAAP EPS: $0.81 (vs. $0.89 previous quarter), below market expectations of $0.93, primarily due to H20-related losses. Excluding this impact, adjusted EPS would have been $0.96.

Revenue projected to reach a new high of $45 billion, reflecting approximately $8 billion in H20 revenue loss due to export control restrictions, slightly below market expectations of $45.5 billion. Crucially, gross margin is expected to recover to 71.8% as Blackwell production scales and costs optimize, aligning with management's previous guidance of margins in the "low-seventies" range during early production phases, with expectations to maintain around 75% by year-end.

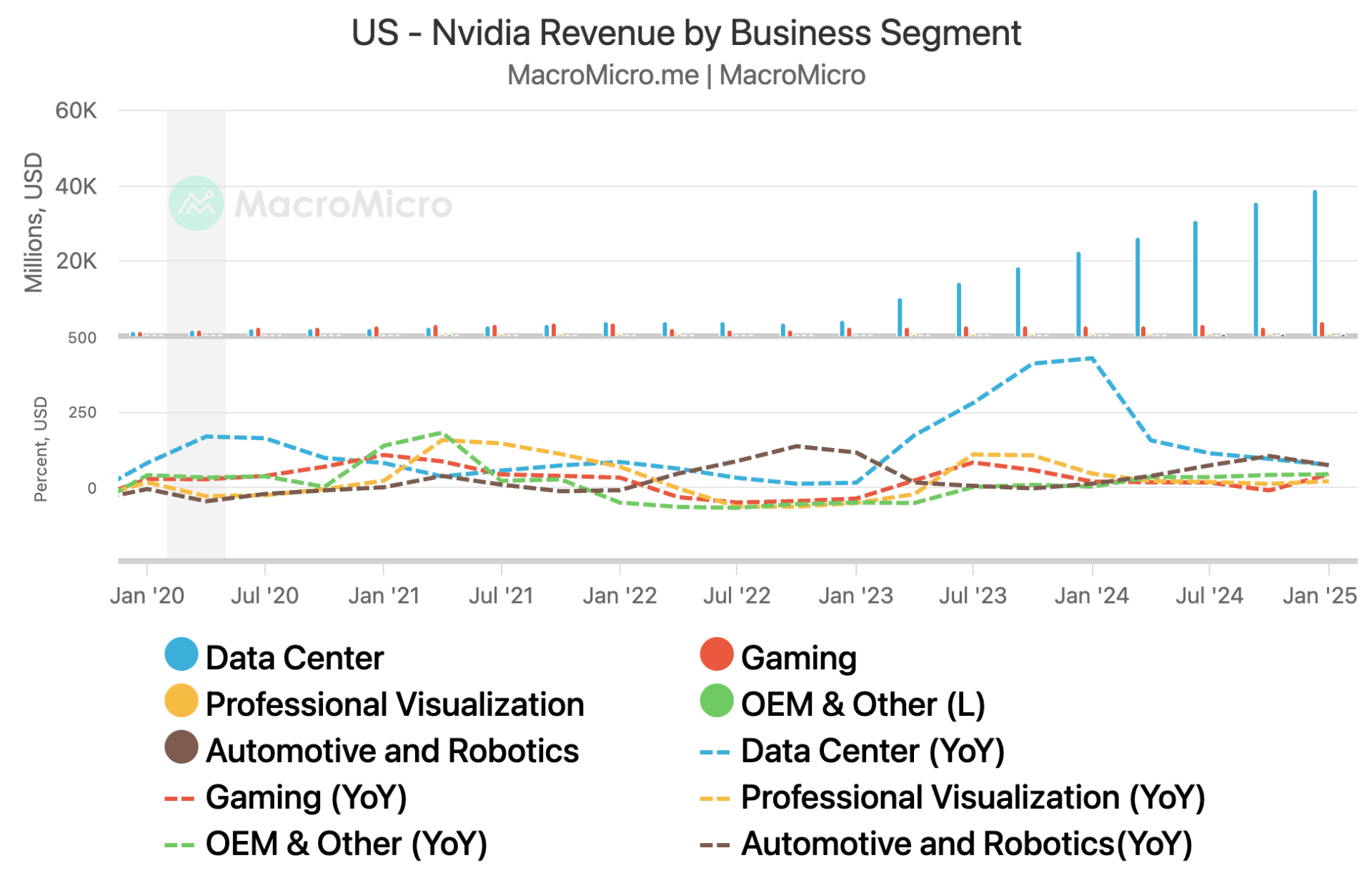

2. Data Center Dominates, Gaming Rebounds, Robotics Sustains

Product segment performance reveals continued diversification strength:

- Data Centers continue as the primary growth engine with revenue of $39.1 billion, up 10% quarter-over-quarter and 73.3% year-over-year (down from 93.3% in the previous quarter but still demonstrating robust growth).

- Gaming showed remarkable recovery with 43.6% year-over-year growth (versus -11.2% in the previous quarter) following the successful launch of the 50-series graphics cards, indicating strong consumer demand recovery.

- Automotive & Robotics maintained elevated performance at $567 million after significant growth in the previous quarter, with year-over-year growth remaining strong at 72.3% (down from 102.8% but still robust). Management remains highly optimistic about the robotics era, projecting billions of robots, hundreds of millions of autonomous vehicles, and hundreds of thousands of robotic factories and warehouses in the future.

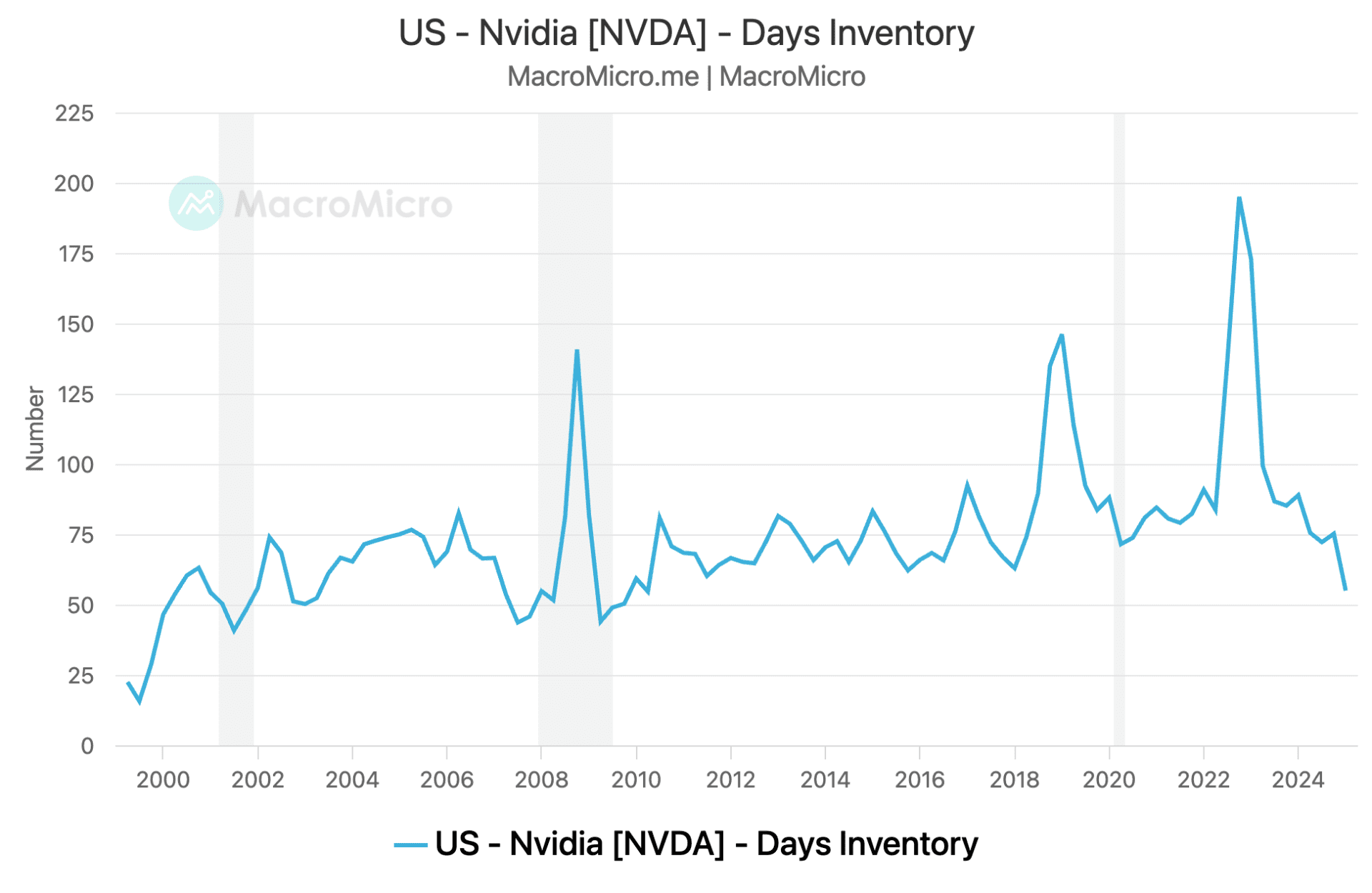

3. Days Sales of Inventory: A Key Indicator for Assessing AI Bubble Risk

"Days sales of inventory (DSI)" remains a critical barometer for evaluating whether the booming AI market might be facing demand weakness or oversupply risks. Higher inventory levels could potentially signal bubble conditions.

NVIDIA’s DSI reached a new record low of 55 days (down from 75.2 days in the previous quarter), representing the most efficient inventory management in company history.

This trend powerfully underscores the sustained and robust demand for AI-related products, with NVIDIA able to convert inventory to sales faster than ever before.

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »