Our MacroMicro Q3 Economic Outlook provided critical insights into the evolving global economic landscape. The discussion centered on the impacts of US tariff policies, Trump's fiscal and monetary strategies, and the potential for a long-term global capital rotation. Despite short-term uncertainties from tariffs and market volatility, the outlook emphasizes a stabilizing global economy, with selective opportunities in non-US markets like India and Taiwan, driven by productivity and strategic positioning.

1. Tariffs Move Toward Moderation, Averting Deep Recession

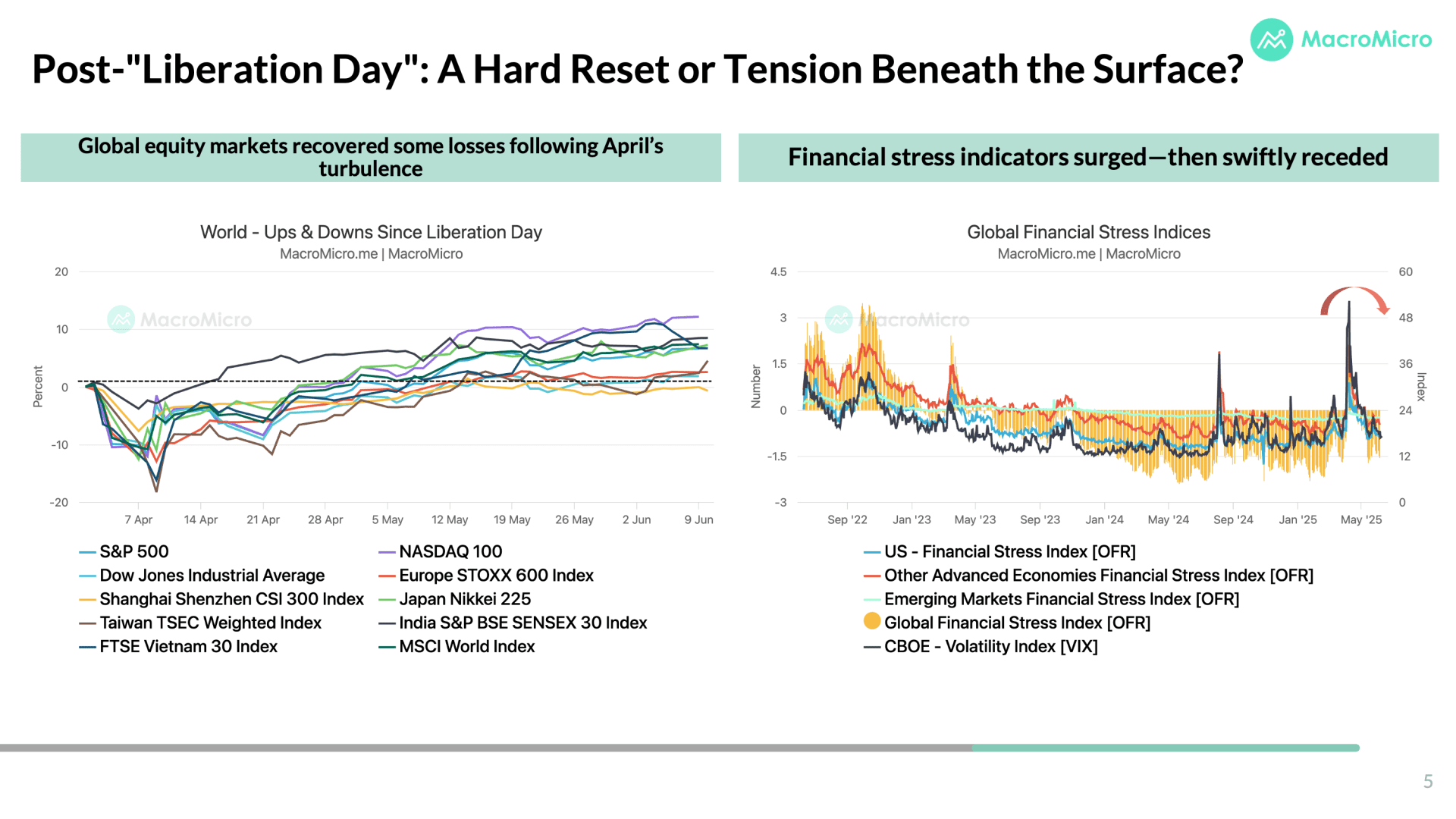

Trump's initial high tariff proposals in April sparked market turmoil, but recent adjustments show a shift toward rationality. Negotiations with economies like the UK, India, and Taiwan have led to lower tariff rates (around 10-15%), reducing the risk of a deep global recession. The trade uncertainty index is declining, and industries with complex supply chains, like automobiles and AI equipment, are seeing exemptions, suggesting a one-time inflationary shock rather than sustained stagflation.

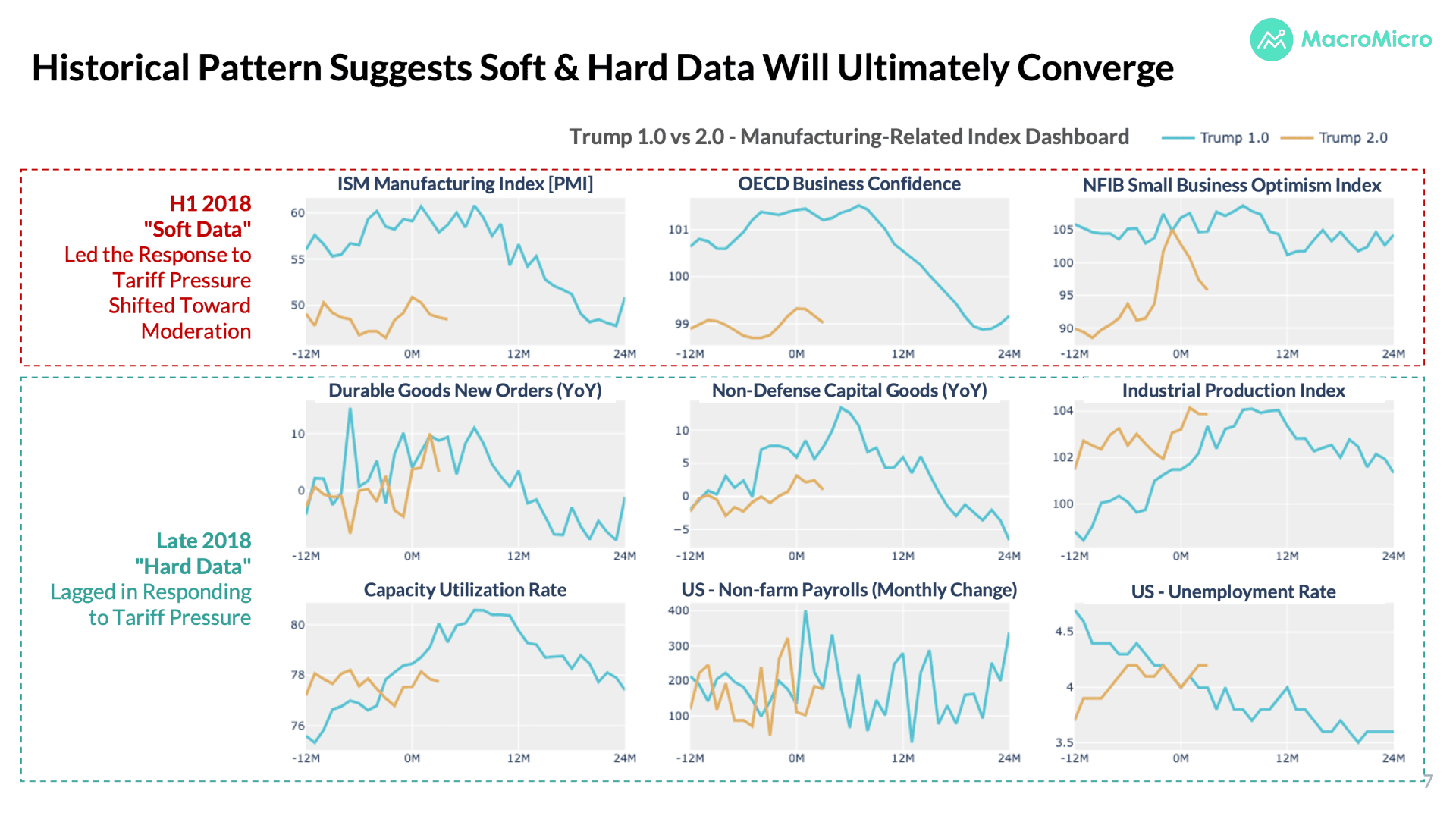

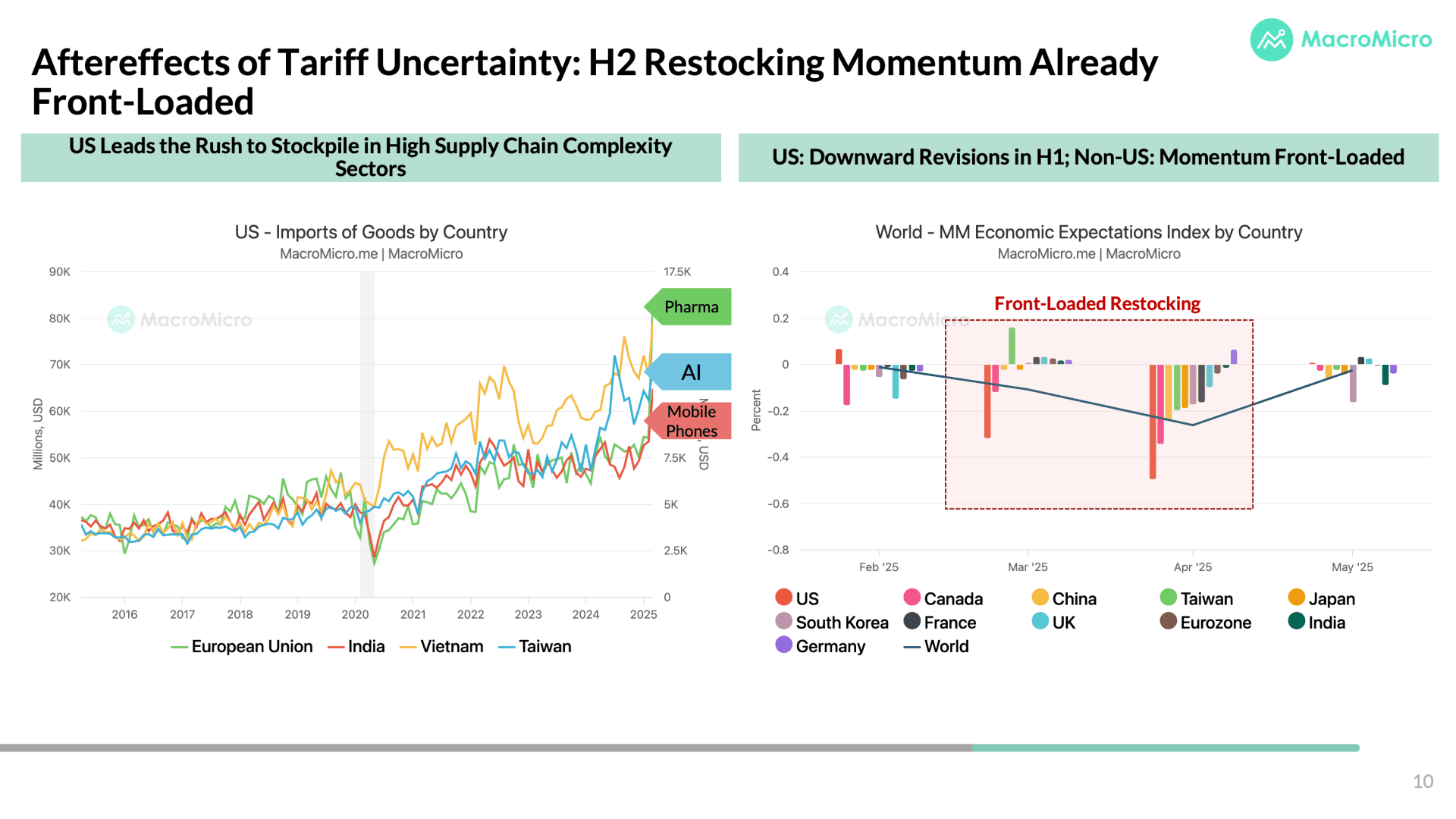

2. Stockpiling Drives Short-Term Export Surge but Risks Inventory Overhang

The second quarter saw a divergence between soft data (e.g., declining business and consumer confidence) and hard data (e.g., robust exports). Early stockpiling in industries like pharmaceuticals and AI equipment boosted exports in economies like Taiwan, but this may lead to inventory pressure in the second half of 2025 if consumption doesn't keep pace. US retail sales grew over 5% annually, but consumption contributed only 0.8% to Q1 GDP, signaling potential slowdown risks.

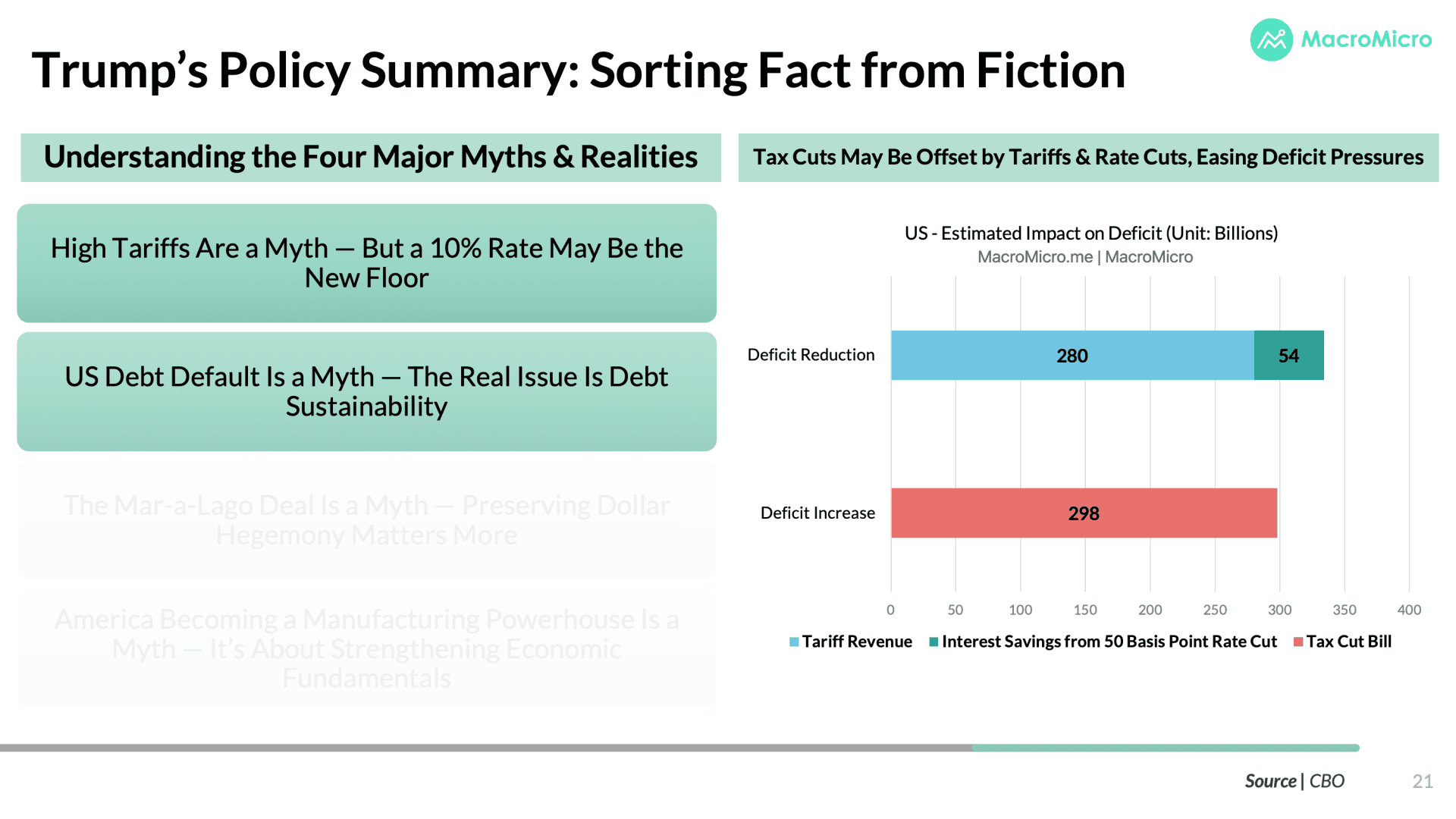

3. Trump's OBBBA Expands Fiscal Policy, Offset by Tariff Revenues

Trump's One Big Beautiful Bill Act (OBBBA) focuses on expanding fiscal policy, including a proposed $3 trillion tax cut bill over the next decade, potentially pushing US debt above 120% of GDP. However, tariff revenues, estimated at $2.5 trillion over the same period, are expected to offset a significant portion of these expenditures, with potential Federal Reserve rate cuts further easing fiscal pressures, though the debt ceiling expiration in Q3 2025 remains a concern.

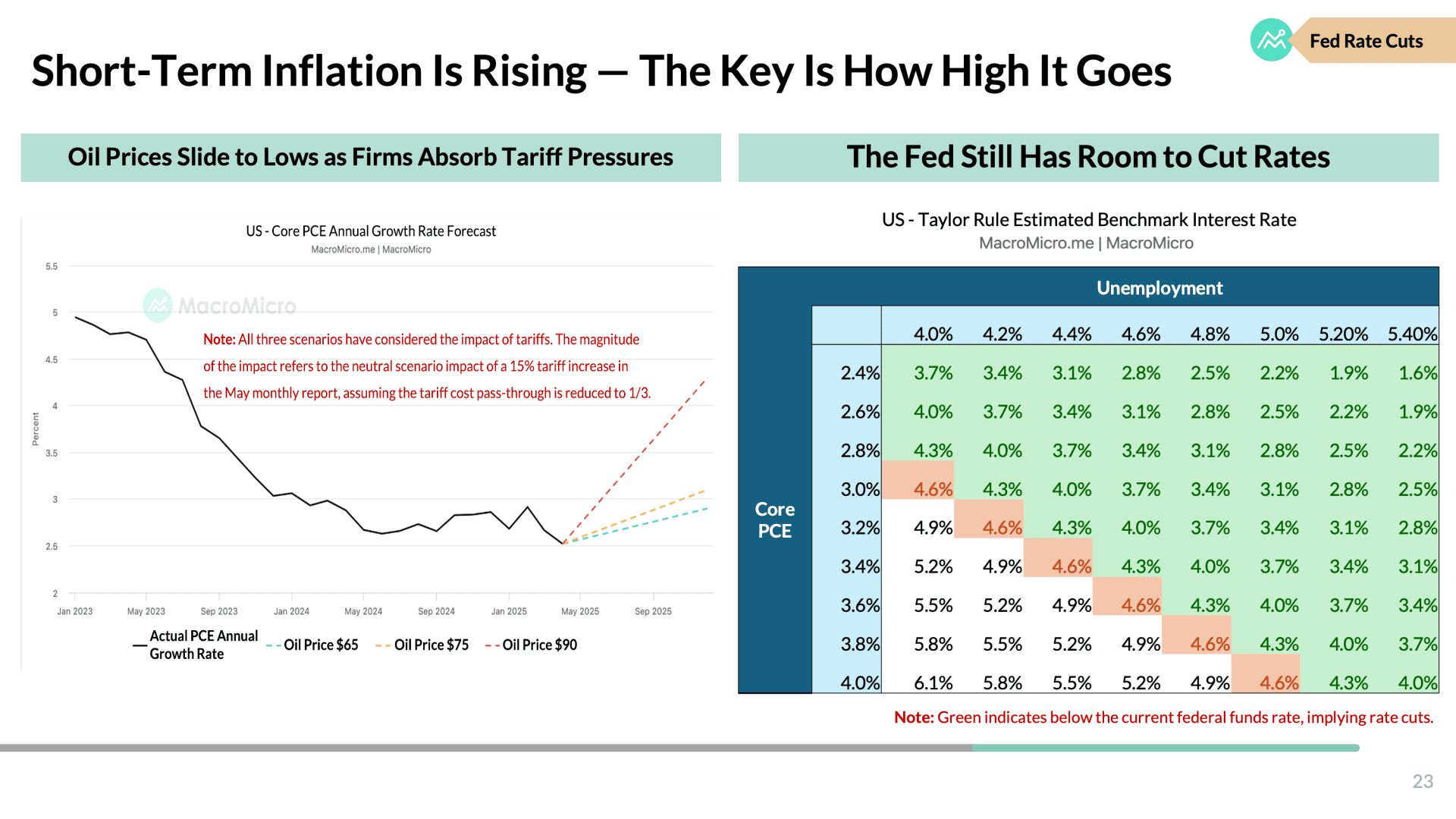

4. Federal Reserve Has Room for Precautionary Rate Cuts

Stable employment (4.2% unemployment rate) and controlled inflation (CPI at 2.3%, core CPI at 2.8%) give the Federal Reserve flexibility to maintain current rates. However, rising vulnerabilities in manufacturing and employment may necessitate rate cuts in late Q3 or Q4 2025. A 10-15% tariff rate could push CPI to around 3%, still within a controllable range, supported by low oil prices and manufacturer cost absorption.

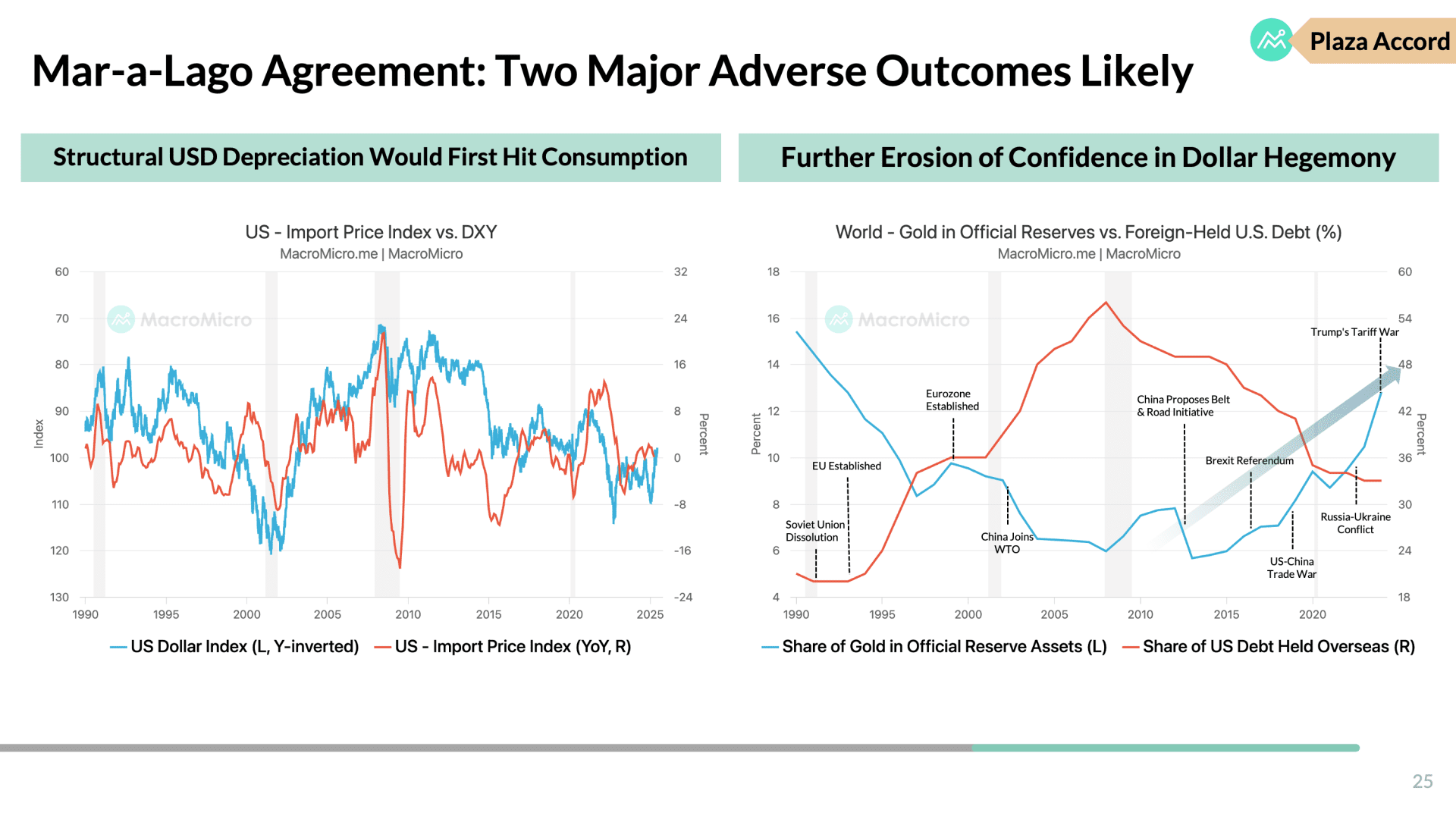

5. US Dollar Hegemony Persists Despite Weakening Confidence

The US dollar index weakened below 100, reflecting declining confidence in dollar assets. Proposals like the Mar-a-Lago agreement to devalue the dollar are unlikely, as they risk undermining dollar hegemony and increasing import prices. Maintaining confidence in the dollar is critical for US fiscal and monetary policies, making deliberate devaluation a low-priority goal.

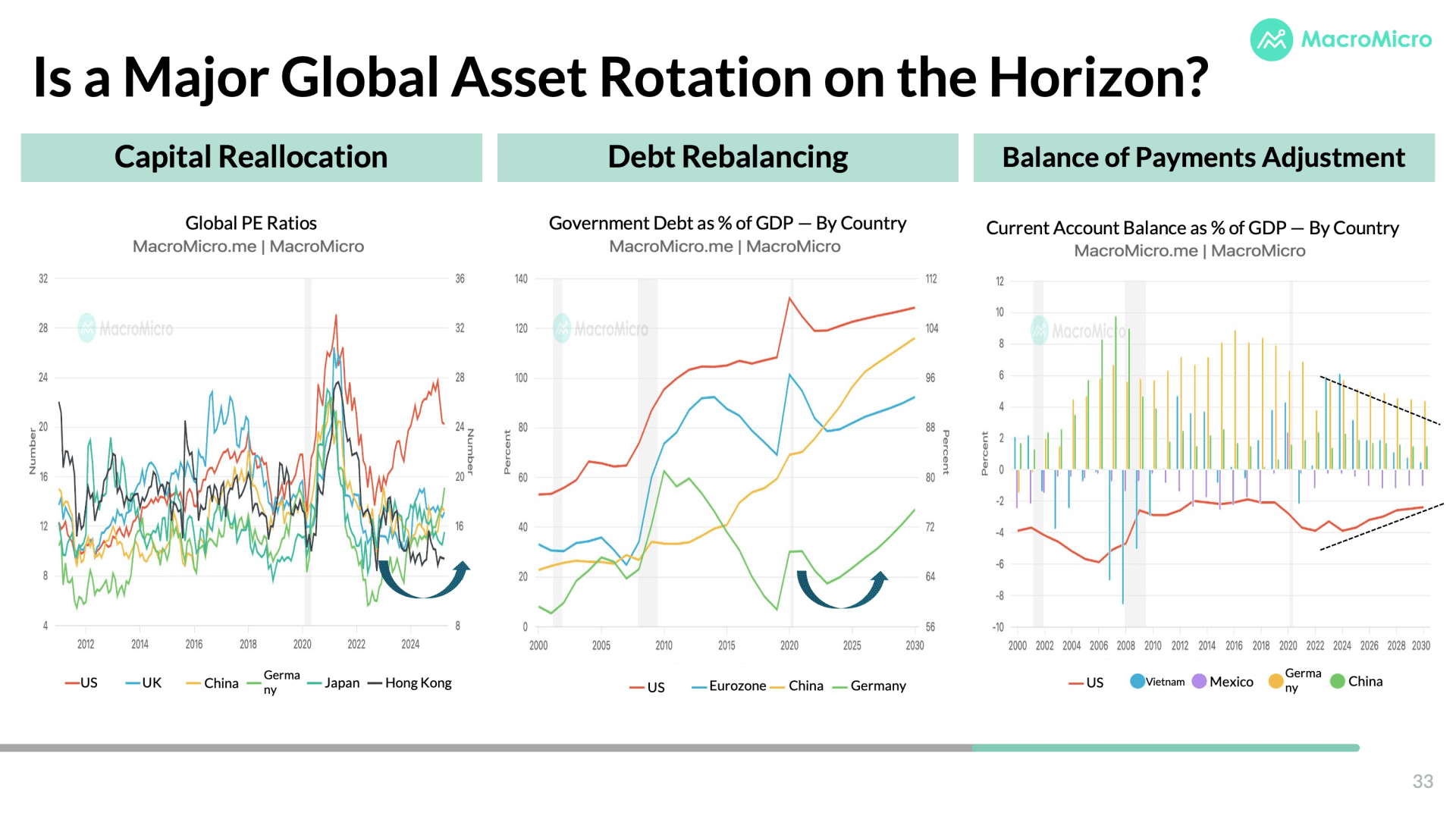

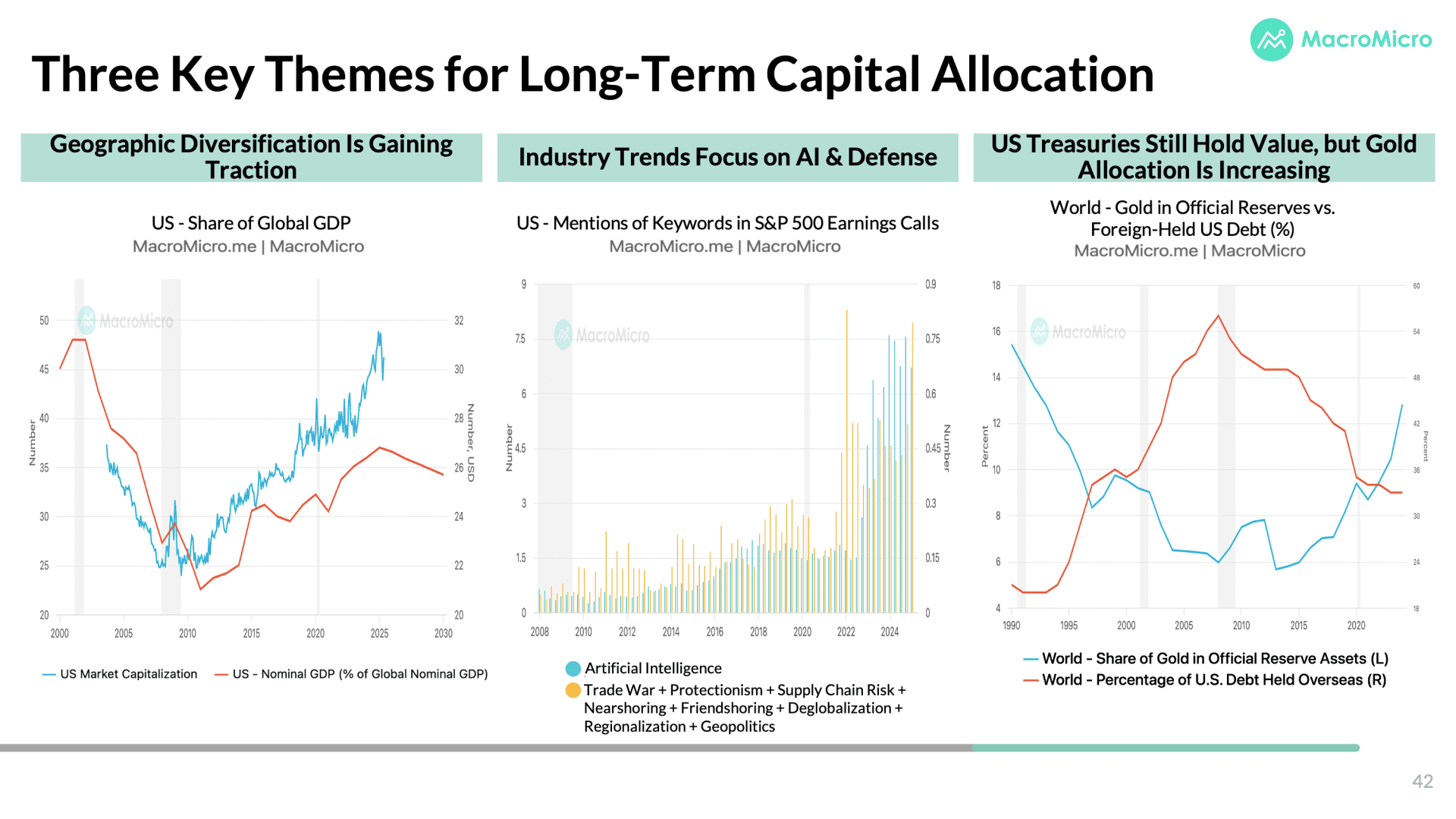

6. Global Capital Shifts to Non-US Markets Like Hong Kong and Europe

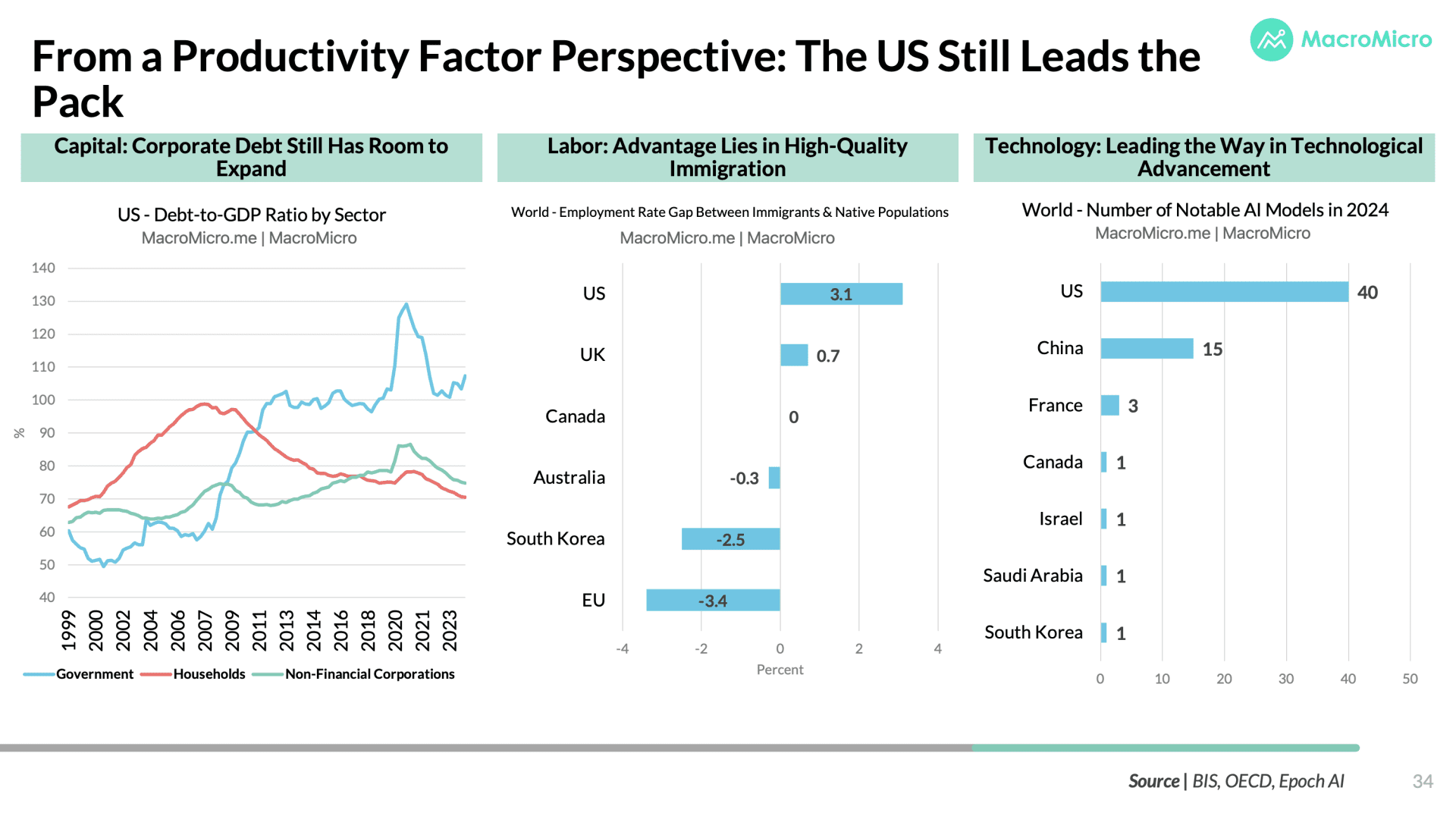

US stock valuations have stagnated, while non-US markets, particularly Hong Kong and European stocks, are rising, signaling a potential global capital rotation. This shift is driven by declining US exceptionalism and increasing fiscal stimulus in Europe and China. However, the US retains a productivity edge, suggesting rotation without a long-term decline in US markets.

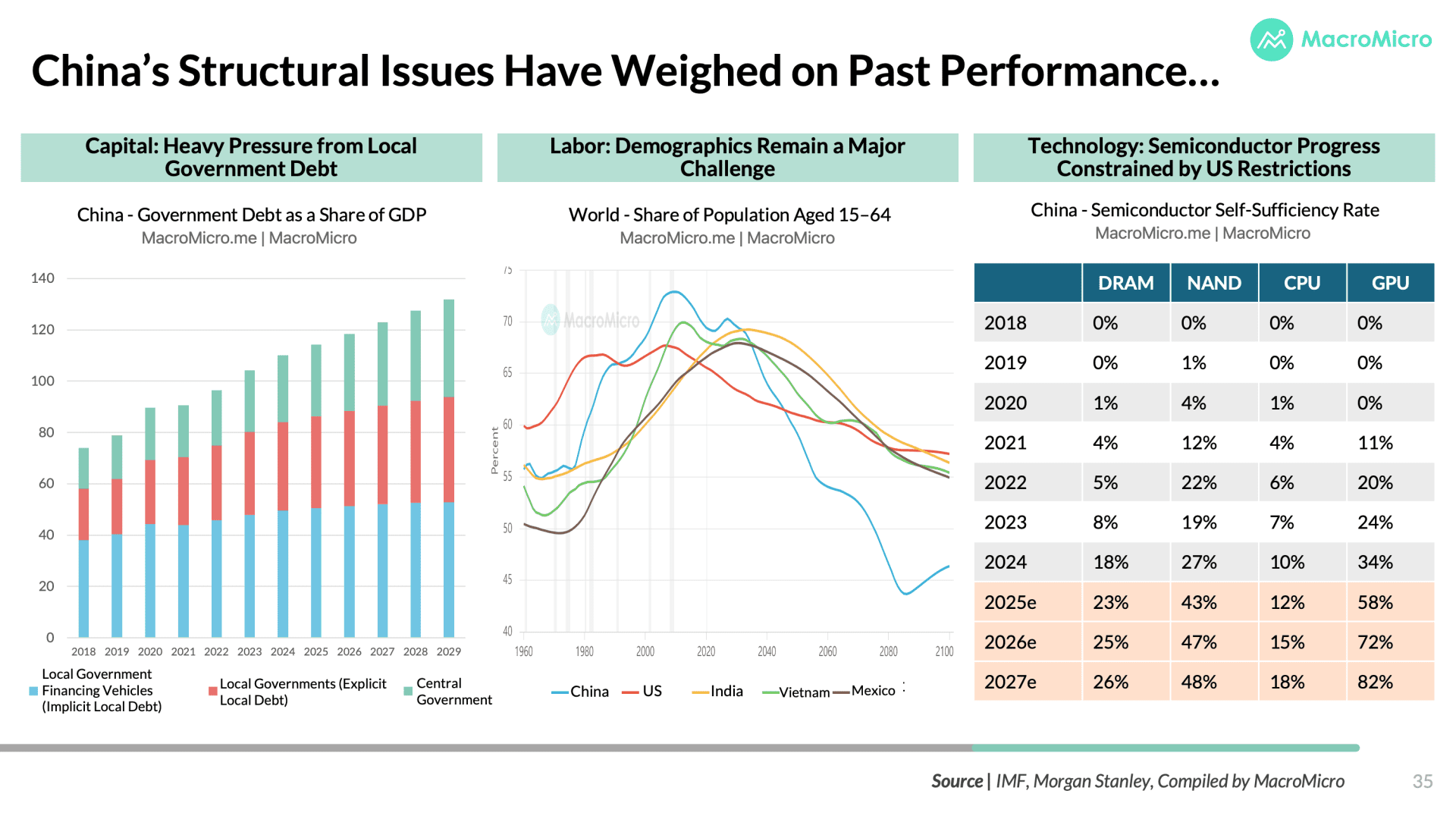

7. China’s Reforms Progress but Growth Potential Remains Constrained

China's central government is increasing fiscal stimulus (2.9 trillion yuan) and refinancing local debt, signaling structural adjustments. However, capital controls, a declining working-age population, and US tech restrictions limit its potential to surpass the US. China's neutral investment outlook reflects progress but significant structural challenges.

8. Diversify Portfolios with US Treasuries, AI Stocks, & Gold

US Treasuries remain a core fixed-income asset despite volatility, outperforming European and Chinese bonds due to liquidity and hegemony. AI-related sectors (e.g., electricity, defense) offer growth potential, while gold remains attractive due to geopolitical risks and central bank purchases. A diversified portfolio of stocks, bonds, and gold is recommended for long-term stability.

As the dust settles from H1’s policy shocks, the contours of the macro landscape are coming into sharper focus—but the path forward is far from linear. From frontloaded trade impacts and fiscal recalibrations to a shifting Fed calculus and the reawakening of non-US equity markets, the second half of 2025 demands more than headlines and hot takes—it requires structured insight, forward-looking frameworks, and global perspective.

That’s what we aim to provide in every MacroMicro Economic Outlook, and it’s what MM Max was built for.

🎥 MM Max members can now stream the full Q3 MEO replay

From livestream replays and premium reports to tools that track macro shifts in real time, MM Max equips you with the clarity and depth that navigating today’s financial landscape demands. If you’re ready to cut through the noise and stay one step ahead, upgrade to MM Max Annual and gain full access to our insights, every step of the way.

Subscribe to MM Max Annual now!

Already a subscriber? Click here to log in.

Full Access to Our Services

Comprehensive data at your service

with key indicators for investment insights

Exclusive flash reports

on key events and data

Create your own charts and analysis

including performance backtesting

Hub of professionals to engage

in meaningful discussions and insights

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »