With over 90% of S&P 500 companies now reporting Q1 2025 results, this earnings season tells a compelling story of corporate resilience amid policy uncertainty. Despite heightened concerns over trade tensions, 77% of companies exceeded earnings per share expectations, driving projected EPS growth above 13% year-over-year. As recent tariff negotiations trend toward de-escalation, US equities have rebounded to levels not seen since February. Yet the critical question remains: how are corporate leaders positioning for the future?

Our analysis of Q1 earnings reveals three dominant themes shaping management priorities, while highlighting the sectors demonstrating the strongest profit momentum. We examine how policy uncertainties continue to influence corporate fundamentals and explore what the data reveals about the sustainability of this earnings recovery; all leveraging insights from advanced analytics tools to dissect corporate priorities and market dynamics.

This report leverages data from MacroMicro’s Industry Intelligence Hub and our newly launched U.S. Earnings Database. Now is the perfect time to upgrade—get 42% OFF the MM Annual Plan, our best offer yet! Join now to unlock powerful macro, industry, and equity insights—all in one platform.

Key Points

- Three Key Management Trends: “Tariffs” concerns have surged to historic highs, particularly in industrial, materials, and consumer sectors; mentions of “recession” have rebounded, but text mining reveals an overall optimistic corporate sentiment, supported by solid economic data and trade negotiation progress; “artificial intelligence” (AI) enthusiasm remains strong, with declining model inference costs driving enterprise AI adoption to 40%.

- 77% of Companies Beat EPS Expectations, with healthcare and communication services showing the strongest profit momentum. The S&P 500 Q1 EPS growth rate started low but gained traction, turning Citigroup’s Earnings Revision Index positive for the first time in 21 weeks, signaling a return of risk-on sentiment. Tariff uncertainties currently weigh most heavily on the 2025 profit outlook for energy and consumer sectors.

- Healthcare faces dual headwinds from Trump's "Most Favored Nation" drug pricing policy targeting 30-80% cost reductions and potential drug tariffs that could compress pharmaceutical margins and R&D budgets. Technology sector shows resilience with AI demand remaining robust, though broader semiconductor outlook faces H2 uncertainty despite current tariff exemptions. NVIDIA's 5/28 earnings will be key, with consensus expecting $43.1B revenue (+65.5% YoY) driven by strong data center and emerging robotics growth.

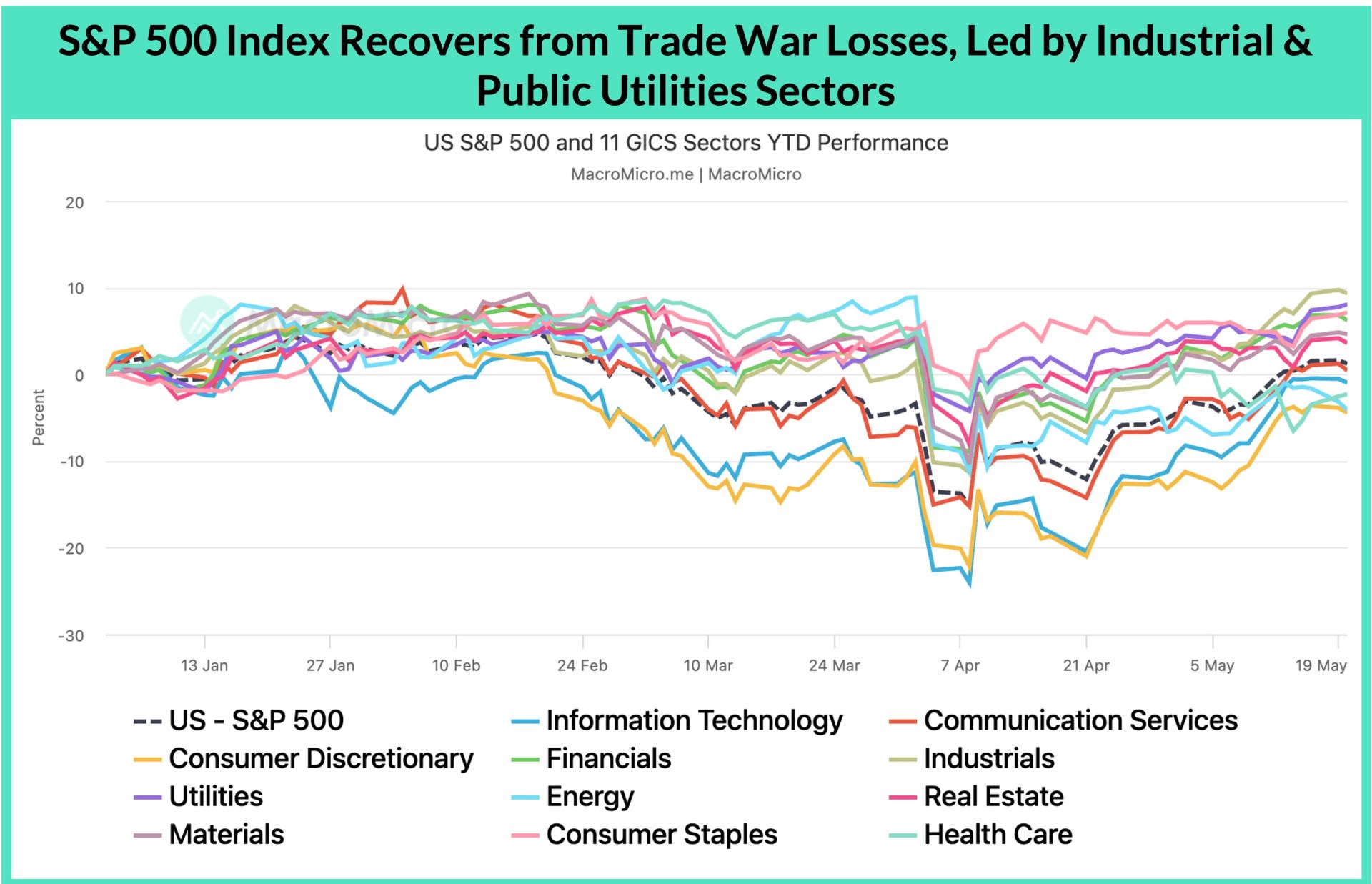

Over 90% of S&P 500 companies have announced their 2025 Q1 earnings, with 77% surpassing market EPS expectations. After adjusting for non-recurring items, the EPS growth rate is expected to reach 13% (down from 16.5% previously), marking two consecutive quarters of double-digit growth and sustained profitability. Following signs of de-escalating tariff tensions, the S&P 500 has reclaimed lost ground, nearing its February all-time high, with industrial and utility sectors leading gains, driven by manufacturing reshoring and AI data center-driven power demand growth.

From a fundamental perspective, tariff uncertainties have eased slightly but persist. How will the 2025 full-year US earnings outlook evolve? Which of the 11 major industry sectors face greater impacts, and which demonstrate resilience? How can investors track management priorities using the Industry Intelligence Hub and our newly launched U.S. Earnings Database? How will upcoming semiconductor and pharmaceutical tariff policies affect the two fastest-growing industries? This report provides a comprehensive analysis.

I. Three Key Corporate Focus Areas: Tariffs, Recession, AI

Analysis of earnings call transcripts reveals three dominant themes shaping corporate strategies: tariffs, recession risks, and artificial intelligence (AI). By applying text mining to thousands of call transcripts, our Industry Intelligence Hub allows researchers to track shifts in management focus with precision, identifying keyword frequency and sentiment to gauge strategic priorities.

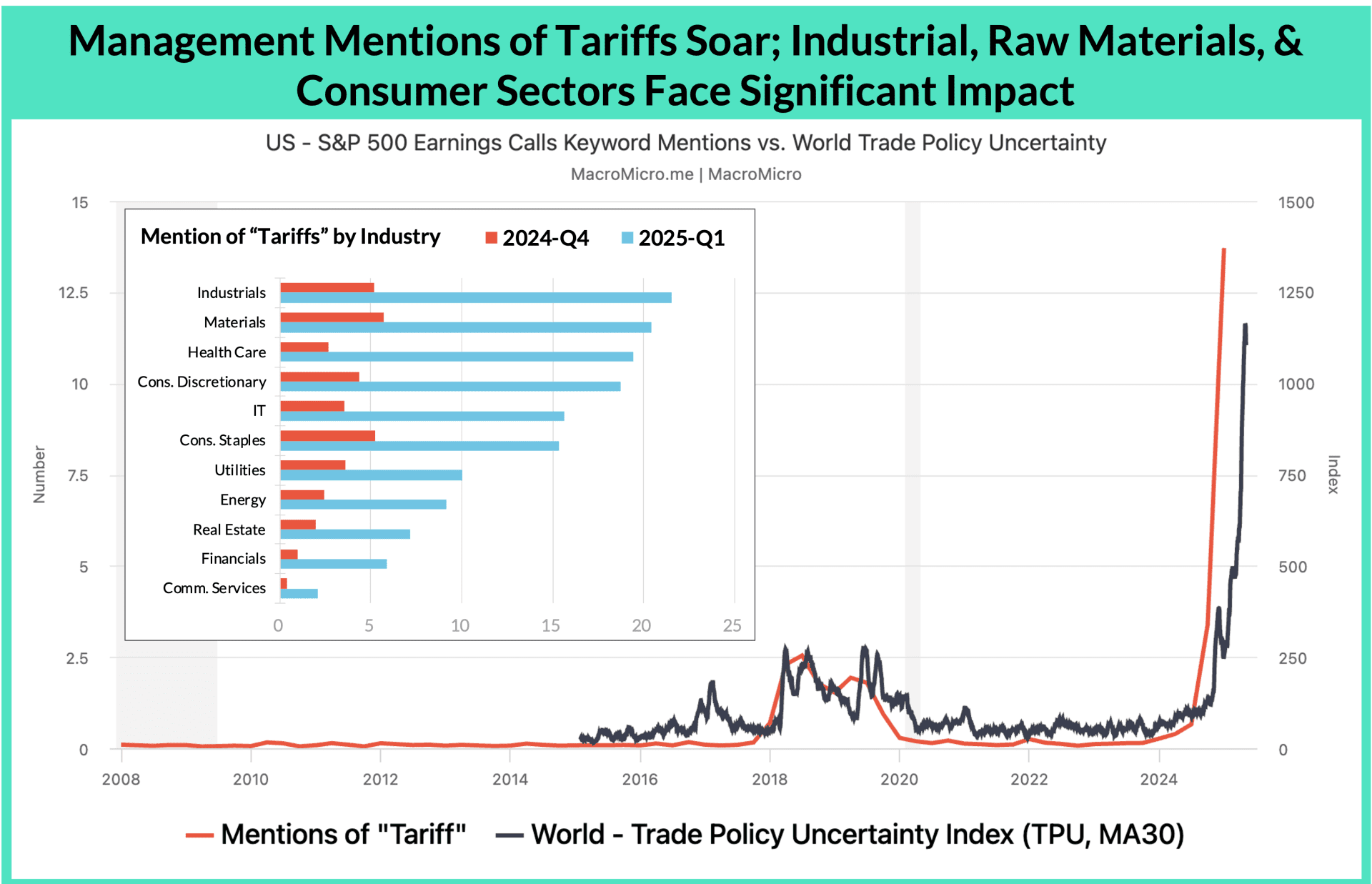

1) “Tariffs” Concerns Surge, with Industrial, Materials, and Consumer Sectors Most Exposed to Overseas Production and Lacking High-Margin Protection

Despite the May 12 Geneva trade statement announcing a 90-day tariff truce between the US and China, which has alleviated some trade uncertainties, corporate concerns about tariff risks remain undeniable. On average, companies mentioned tariff-related terms over 13 times per call, a record high, compared to a peak of just 2.5 times during Trump 1.0 in 2018. This underscores the broader scope and deeper economic, trade, and supply chain disruptions of the current tariff environment.

Industrial, materials, healthcare, and discretionary consumer sectors mentioned tariffs most frequently. While pharmaceuticals are currently under Section 232 tariff investigations and remain exempt, the other three sectors heavily rely on overseas production. According to a 2022 US Bureau of Economic Analysis (BEA) study, approximately 20% of US manufacturing gross output comes from abroad, with the highest proportions in primary metals (26%), machinery (21%), electrical equipment and components (21%), textiles (20%), and plastics/rubber (20%). Additionally, industrial, materials, and consumer sectors generally lack high-margin protection, with 2024 net margins averaging 9.8%, below the S&P 500’s 14% and far below the tech sector’s 26%.

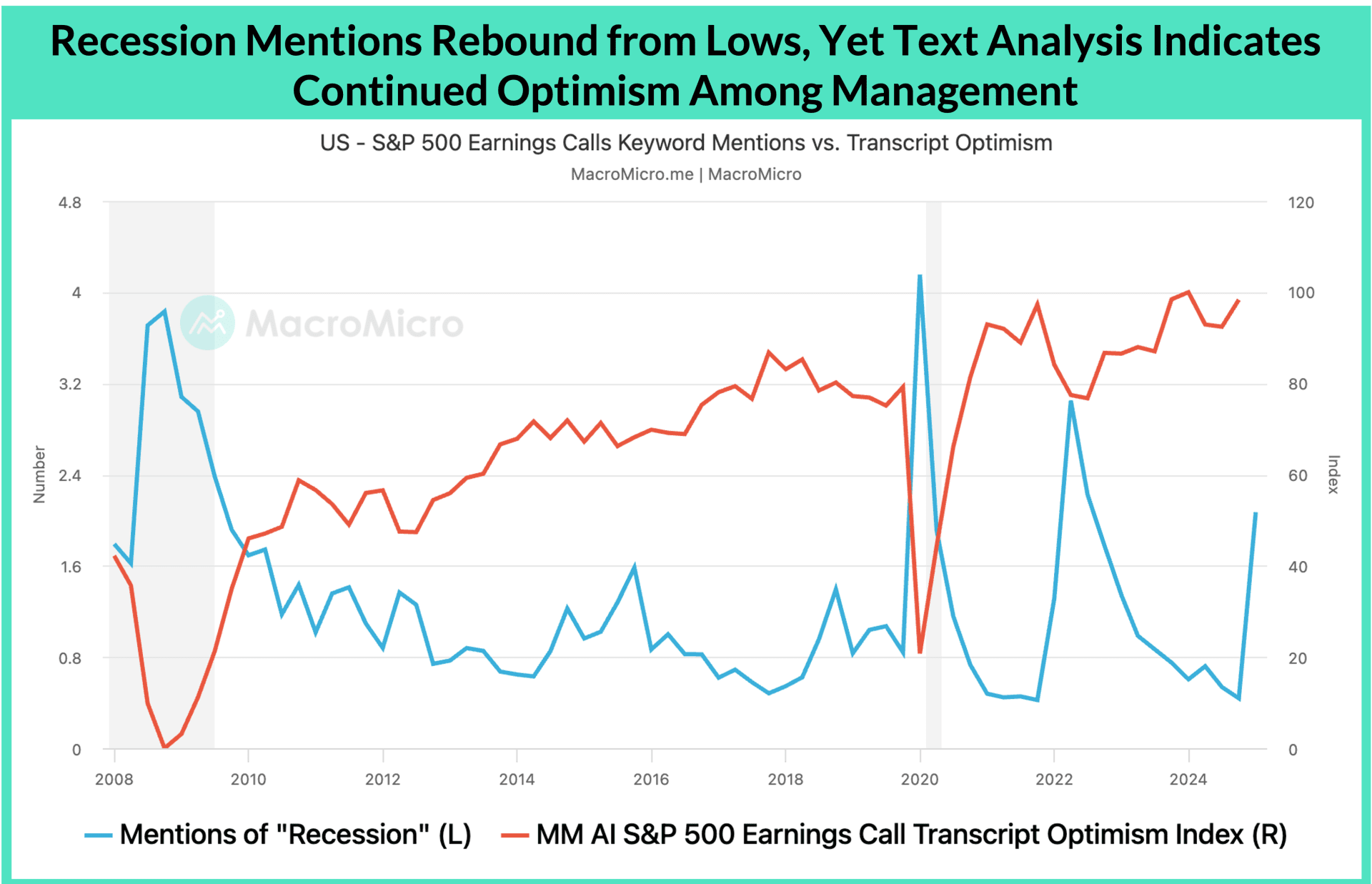

2) “Recession” Mentions Rebound, but Corporate Optimism Persists

Beyond tariffs, “recession” mentions rose sharply from 0.44 times per call in Q4 2024 to 2.07 in Q1 2025, though still below peaks during the 2022 Russia-Ukraine conflict and 2020 COVID-19 pandemic. Are corporate recession concerns warranted? Soft data, such as the May University of Michigan Consumer Confidence Index dropping to 50.8 (the second-lowest since 1978, only above June 2022’s 50.0), signals weakness. However, NBER recession indicators remain near zero, retail sales maintain above 5% growth, supported by dining and healthcare services alongside auto exports, and improving tariff negotiations reduce the likelihood of a deep recession.

When paired with MacroMicro's AI Earnings Call Optimism Index, corporate sentiment remains broadly positive. For instance, S&P Global (SPGI) stated in its latest call, “We expect GDP growth to be below forecasts but do not anticipate a recession.” Marriott International (MAR) noted, “We are not assuming a recession and expect global demand to remain strong.” While both mentioned “recession,” their outlooks were positive. By sector, communication services, utilities, healthcare, and real estate remain optimistic, while materials, industrial, consumer, and financial sectors are relatively pessimistic.

3) “Artificial Intelligence” Enthusiasm Grows, DeepSeek Concerns Fade

Despite market focus on tariffs and recession risks over the past two months, mentions of “artificial intelligence” reached new highs, surprising given the January disruption caused by DeepSeek’s low-cost R1 inference model impacting hardware tech stocks.

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »