Executive Summary:

Trump’s Liberation Day last Wednesday triggered Annihilation Days on Thursday and Friday, with the Stock Market Vigilantes giving a costly thumbs-down to Trump’s Reign of Tariffs. Trump officials say they aim to make Main Street wealthy again even if that’s bad for Wall Street. The problem is that Main Street owns lots of equities traded on Wall Street, so the two streets prosper and suffer together. Congress can’t do much to stop Trump given his veto power, but he might get the message that hurting Main Street’s stock portfolios can cause a recession and jeopardize the GOP majority in Congress. If so, he might postpone the reciprocal tariffs, giving trade negotiations time to work. Also, the courts might block Trump’s tariffs. An early end to Trump’s tariff nightmare would result in a V-shaped stock-market bottom. We’re counting on that; the alternative is just plain ugly. … Check out the accompanying chart collection.

Trump’s Tariffs I: President’s Exit Ramp.

So far, congressional Republicans are giving Trump Tariffs 2.0 the benefit of the doubt. Some are voicing their concerns. A few Senate Republicans are joining the Democrats in the Senate to support a bill to cancel Trump’s tariffs on Canada. But it won’t pass in the House, and Trump has already said that he won’t sign it.

Meanwhile, the Stock Market Vigilantes aren’t giving Trump Tariffs 2.0 the benefit of the doubt. The S&P 500 and the Nasdaq plunged 9.9% and 10.7% from April 1, i.e., the day before Liberation Day through Friday’s close.

▌View Related Live Charts: US - S&P 500

▌View Related Live Charts: US - S&P 500

▌View Related Live Charts: US - NASDAQ Composite

▌View Related Live Charts: US - NASDAQ Composite

They are now down 17.4% and 22.7% from their respective record highs on February 19 and December 16.

In other words, Liberation Day has been followed by Annihilation Days in the stock market.

On Saturday morning, I nearly gagged on my bagel listening to a CNN interview with Peter Navarro. The President’s senior counselor for trade and manufacturing declared that the tariffs are aimed at benefiting Main Street, not Wall Street. Other senior officials in the Trump administration, including Treasury Secretary Scott Bessent, have said the same.

I have news for them: Wall Street is Main Street. Wall Street matters a great deal to Main Street. Main Street owns lots of stocks in American corporations that are facing massive disruptions as a result of Trump Tariffs 2.0. Navarro predicted that the stock market will bottom “soon” and that the stock market rally will broaden to include the S&P 493 and not just the Magnificent 7. Navarro also predicted that the Dow Jones will rise to 50,000 by the end of Trump’s term. He implored the media to accentuate the positives of Trump’s tariffs. In fact, the media was just as surprised by last week’s stock market rout as were Wall Street and Main Street.

Congress is about to get an earful. Main Street undoubtedly will voice our anger about the immediate adverse effects of Trump’s tariffs on our investment and retirement portfolios. Senior citizens who have retired or were planning to do so must be especially mad. The administration’s response is that the short-term pain will be worth the long-term gain. The problem is that Americans don’t do pain very well and aren’t convinced that the eventual gain will be worth it. So the pressures on congressional representatives from their constituencies to stop the tariff madness will be intense in coming days, especially if the stock market continues to crash.

Trump needs an exit strategy. The obvious one is for him to declare victory. He can keep his 10% base tariff on imports from all countries while delaying implementation of the reciprocal tariffs on countries that agree to negotiations. The stock market undoubtedly would rebound sharply if he were to do that.

There is some good news regarding tariffs. The Vietnamese reportedly are ready to drop their 90% tariffs. Argentina wants to go down to 0%. India and South Korea are negotiating with the White House. In February, the European Union considered dropping its auto tariff from 10.0% to 2.5%, and offered to buy American energy and weaponry to avoid Trump’s tariffs. Now, however, the EU is planning countermeasures to the new US tariffs. That could be the next shoe to drop on the stock market. Indeed, the EU was already finalizing a first package of tariffs on up to €26 billion ($28.4 billion) of US goods for mid-April in response to the US's steel and aluminum tariffs that took effect on March 12.

Meanwhile, as I noted in Friday’s QuickTakes, Trump’s tariffs are bound to be challenged in courts:

(1) The first case has been started by the New Civil Liberties Alliance (NCLA) on behalf of a small retail stationery business named “Simplified.” Bloomberg reported: “The lawsuit filed in federal court in Florida may be the first legal challenge to the sweeping new US tariffs. ... ‘By invoking emergency power to impose an across-the-board tariff on imports from China that the statute does not authorize, President Trump has misused that power, usurped Congress’s right to control tariffs, and upset the Constitution’s separation of powers,’ Andrew Morris, senior litigation counsel at NCLA, said in a statement announcing the suit. The complaint seeks a court order declaring the tariffs unconstitutional and finding that they were adopted in violation of US administrative rules.”

(2) Other business groups are considering similar challenges. Politico reports: “At issue is a nearly-50-year-old law, the International Emergency Economic Powers Act, that Trump is citing to impose both the duties on China and the global ‘reciprocal tariffs’ he announced this week. The 1977 law gives the president broad authority to respond to a national emergency. But Trump is the first president to use it to impose tariffs, which is a power the U.S. Constitution assigned to Congress.”

Might the Fed come to the rescue and provide enough monetary easing to offset the deflationary consequences of Trump’s tariffs? On Friday, Trump posted the following on Truth Social: “This would be a PERFECT time for Fed Chairman Jerome Powell to cut Interest Rates. He is always ‘late,’ but he could now change his image, and quickly. Energy prices are down, Interest Rates are down, Inflation is down, even Eggs are down 69%, and Jobs are UP, all within two months - A BIG WIN for America. CUT INTEREST RATES, JEROME, AND STOP PLAYING POLITICS!”

Also on Friday, shortly after Trump’s plea, Powell told business journalists in Arlington, Virginia, that the Fed is in no hurry to cut the federal funds rate. He said the Fed faces a “highly uncertain outlook” because of Trump’s reciprocal tariffs. He also said that the tariffs announced were “significantly larger than expected.” In his prepared remarks, Powell stated: “Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem. … We are well positioned to wait for greater clarity before considering any adjustments to our policy stance. It is too soon to say what will be the appropriate path for monetary policy.”

In other words, “Fuhgeddaboudit” was Powell’s response to Trump.

That was also Powell’s message to the financial markets. Nevertheless, by the end of trading on Friday, the financial futures market signaled that it expects two to three 25bps rate cuts over the next six months and four to five rate cuts over the next 12 months.

▌View Related Live Charts: US - FedWatch Interest Rate Projections

▌View Related Live Charts: US - FedWatch Interest Rate Projections

▌View Related Live Charts: US - FedWatch Interest Rate Projections

▌View Related Live Charts: US - FedWatch Interest Rate Projections

Trump’s Tariffs II: Nero Golfs.

In his CNN interview Saturday morning, Navarro claimed that thanks to Trump’s policies, the price of oil has dropped sharply, thus reducing the price of gasoline.

▌View Related Live Charts: Brent Crude Oil

▌View Related Live Charts: Brent Crude Oil

▌View Related Live Charts: US - AAA Daily National Average Gasoline Prices

▌View Related Live Charts: US - AAA Daily National Average Gasoline Prices

He also noted that bond yields have dropped, causing mortgage rates to decline.

▌View Related Live Charts: US - 10Y/2Y Treasury Yield Spread vs. Treasury Price

▌View Related Live Charts: US - 10Y/2Y Treasury Yield Spread vs. Treasury Price

▌View Related Live Charts: US - 10Y Treasury Yield vs. Mortgage

▌View Related Live Charts: US - 10Y Treasury Yield vs. Mortgage

He was making the debatable claim that the pain the tariffs are causing for stock investors has been more than offset by the gain of lower gasoline prices and mortgage rates. In addition, he stated that a few companies and countries have recently committed to spend trillions of dollars on capital investments in the US.

The Great Crash during the Great Depression was also accompanied by plunging commodity prices and interest rates. So it is hard to take comfort from last week’s drop in commodity prices and interest rates. The administration can’t take any credit for falling commodity prices and interest rates if the reason they are falling is that the administration’s tariff policies are causing a recession! Capital spending always declines during recessions even if spending commitments were made during good times.

The biggest risk to the economy currently, following last week’s stock market rout, is that the resulting negative wealth effect depresses consumer spending:

(1) Total equity market capitalization.

Data compiled by the Fed show that the total value of stocks traded in the US at the end of 2024 was $93 trillion.

▌View Related Live Charts: MM US Stock Fundamental Index

▌View Related Live Charts: MM US Stock Fundamental Index

At the end of Q1-2025, the total value of the S&P 500 was $50 trillion. So a 10% to 20% drop in this stock index would amount to a loss of $5 trillion to $10 trillion just in the S&P 500. That could have a significant negative wealth effect on US consumer spending, especially by retired and retiring Baby Boomers.

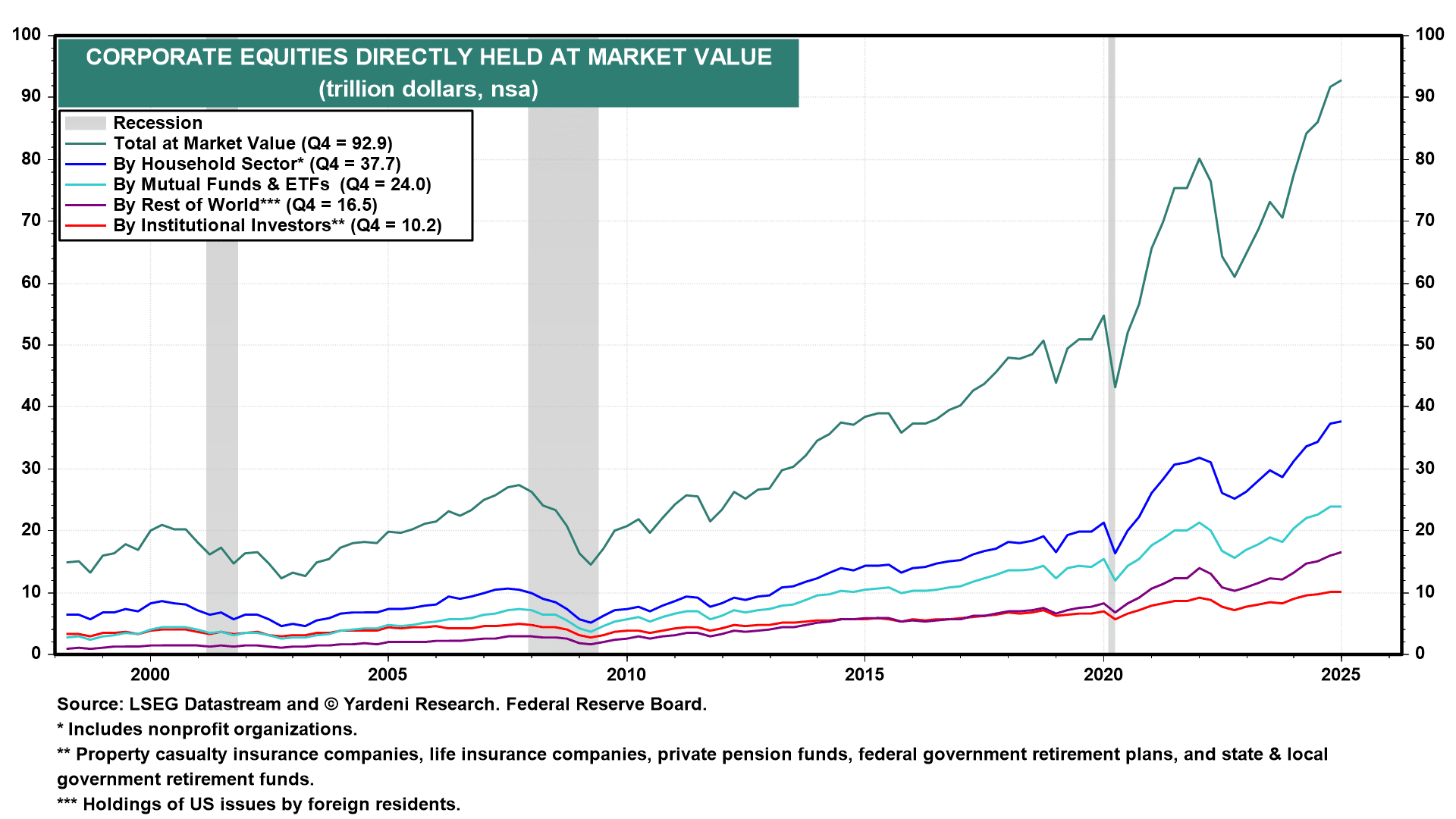

(2) Who owns US equities?

Of the $93 trillion in total equities, American households directly held $38 trillion at the end of Q4-2024. Mutual funds and ETFs held $24 trillion. Institutional investors including life insurance companies, private pension funds, and federal, state & local government retirement funds held $10.2 trillion. The rest of the world held $16.5 trillion.

(3) Households & Baby Boomers.

The Fed also compiles data for the net worth of the household sector excluding nonprofit organizations. At the end of 2024, households held $46.8 trillion in corporate equities and mutual funds.

The Baby Boomers accounted for more than half of that at $25.2 trillion.

At the end of last year, households held a record $15.2 trillion in IRAs.

Altogether, equities as a share of the assets held by households (including NPOs) rose to a record 43.5% during Q4-2025.

This means that they are more exposed to a negative wealth effect from falling stock prices. That’s what is happening on Main Street.

(4) ‘Nero fiddles as Rome burns.’ On Friday, the President went to Trump International Golf Club in West Palm Beach, before attending a fundraising dinner for a super PAC that backs Trump, MAGA Inc. On Saturday, he golfed at his course in Jupiter, where the Senior Club Championships are taking place. The White House reported that Trump “won his second round matchup of the Senior Club Championship ... and advances to the Championship Round tomorrow.”

The President wasn’t negotiating trade deals this weekend. He was too busy relaxing on the links.

Trump’s Tariffs III: Stress Testing a Resilient Economy.

The plunge in stock prices since Liberation Day increases the odds that the resulting negative wealth effect will depress consumer spending, which increases the odds of a recession, which is, in turn, depresses stock prices. The odds of a recession according to Polymarket.com rose to 60% at the end of Friday.

▌View Related Live Charts: US - Probability of Recession in A Year (10Y-3M Model)

▌View Related Live Charts: US - Probability of Recession in A Year (10Y-3M Model)

It was at 42% on April 1.

We raised our subjective probability of a recession this year from 20% to 35% on March 5, and from 35% to 45% on March 31. Along the way, we also slashed our year-end target for the S&P 500 from 7000 to 6000 and cut our projection for 2025 S&P 500 earnings per share from $285 to $260. We also lowered our real GDP growth rate projection for this year from 2.5% to 3.0%, then down to 1.5%.

We expected Liberation Day to bring trouble. So for now, we aren’t changing our outlook or our odds of a recession. Call us delusional optimists, but we aren’t ready to bet against the resilience of the US economy in general or its consumers in particular. Of course, our big assumption is that Trump’s tariff nightmare will go away sooner rather than later, one way or another.

Meanwhile, let’s review the latest signs of the economy’s resilience; we acknowledge that they might be the last ones for a while if the nightmare persists:

(1) Employment. We anticipated a strong rebound in March employment from the depressed gains during January and February, which we attribute to colder-than-normal weather. Nonfarm payrolls rose 228,000 during March.

▌View Related Live Charts: US - Nonfarm Payrolls by Sector (Monthly Change)

▌View Related Live Charts: US - Nonfarm Payrolls by Sector (Monthly Change)

Private services-providing industries increased their payrolls by 197,000. Aggregate weekly hours worked rose to a record 4.6 billion.

(2) Retail sales.

We also expect to see a rebound in March retail sales when it’s reported on April 16. We already know that auto sales jumped 11% m/m during March to 17.8 million units (saar), the highest since April 2021.

▌View Related Live Charts: US - Retail Sales vs. Car Sales

▌View Related Live Charts: US - Retail Sales vs. Car Sales

Some of that rebound undoubtedly reflected buying in advance of price increases resulting from Trump’s tariffs. April’s sales should also be very strong. But after that, sales could go over a cliff unless Tariff Man changes his mind.

Executive Summary:

Trump’s Liberation Day last Wednesday triggered Annihilation Days on Thursday and Friday, with the Stock Market Vigilantes giving a costly thumbs-down to Trump’s Reign of Tariffs. Trump officials say they aim to make Main Street wealthy again even if that’s bad for Wall Street. The problem is that Main Street owns lots of equities traded on Wall Street, so the two streets prosper and suffer together. Congress can’t do much to stop Trump given his veto power, but he might get the message that hurting Main Street’s stock portfolios can cause a recession and jeopardize the GOP majority in Congress. If so, he might postpone the reciprocal tariffs, giving trade negotiations time to work. Also, the courts might block Trump’s tariffs. An early end to Trump’s tariff nightmare would result in a V-shaped stock-market bottom. We’re counting on that; the alternative is just plain ugly. … Check out the accompanying chart collection.

Trump’s Tariffs I: President’s Exit Ramp.

So far, congressional Republicans are giving Trump Tariffs 2.0 the benefit of the doubt. Some are voicing their concerns. A few Senate Republicans are joining the Democrats in the Senate to support a bill to cancel Trump’s tariffs on Canada. But it won’t pass in the House, and Trump has already said that he won’t sign it.

Meanwhile, the Stock Market Vigilantes aren’t giving Trump Tariffs 2.0 the benefit of the doubt. The S&P 500 and the Nasdaq plunged 9.9% and 10.7% from April 1, i.e., the day before Liberation Day through Friday’s close.

▌View Related Live Charts: US - S&P 500

▌View Related Live Charts: US - NASDAQ Composite

They are now down 17.4% and 22.7% from their respective record highs on February 19 and December 16.

In other words, Liberation Day has been followed by Annihilation Days in the stock market.

On Saturday morning, I nearly gagged on my bagel listening to a CNN interview with Peter Navarro. The President’s senior counselor for trade and manufacturing declared that the tariffs are aimed at benefiting Main Street, not Wall Street. Other senior officials in the Trump administration, including Treasury Secretary Scott Bessent, have said the same.

I have news for them: Wall Street is Main Street. Wall Street matters a great deal to Main Street. Main Street owns lots of stocks in American corporations that are facing massive disruptions as a result of Trump Tariffs 2.0. Navarro predicted that the stock market will bottom “soon” and that the stock market rally will broaden to include the S&P 493 and not just the Magnificent 7. Navarro also predicted that the Dow Jones will rise to 50,000 by the end of Trump’s term. He implored the media to accentuate the positives of Trump’s tariffs. In fact, the media was just as surprised by last week’s stock market rout as were Wall Street and Main Street.

Congress is about to get an earful. Main Street undoubtedly will voice our anger about the immediate adverse effects of Trump’s tariffs on our investment and retirement portfolios. Senior citizens who have retired or were planning to do so must be especially mad. The administration’s response is that the short-term pain will be worth the long-term gain. The problem is that Americans don’t do pain very well and aren’t convinced that the eventual gain will be worth it. So the pressures on congressional representatives from their constituencies to stop the tariff madness will be intense in coming days, especially if the stock market continues to crash.

Trump needs an exit strategy. The obvious one is for him to declare victory. He can keep his 10% base tariff on imports from all countries while delaying implementation of the reciprocal tariffs on countries that agree to negotiations. The stock market undoubtedly would rebound sharply if he were to do that.

There is some good news regarding tariffs. The Vietnamese reportedly are ready to drop their 90% tariffs. Argentina wants to go down to 0%. India and South Korea are negotiating with the White House. In February, the European Union considered dropping its auto tariff from 10.0% to 2.5%, and offered to buy American energy and weaponry to avoid Trump’s tariffs. Now, however, the EU is planning countermeasures to the new US tariffs. That could be the next shoe to drop on the stock market. Indeed, the EU was already finalizing a first package of tariffs on up to €26 billion ($28.4 billion) of US goods for mid-April in response to the US's steel and aluminum tariffs that took effect on March 12.

Meanwhile, as I noted in Friday’s QuickTakes, Trump’s tariffs are bound to be challenged in courts:

(1) The first case has been started by the New Civil Liberties Alliance (NCLA) on behalf of a small retail stationery business named “Simplified.” Bloomberg reported: “The lawsuit filed in federal court in Florida may be the first legal challenge to the sweeping new US tariffs. ... ‘By invoking emergency power to impose an across-the-board tariff on imports from China that the statute does not authorize, President Trump has misused that power, usurped Congress’s right to control tariffs, and upset the Constitution’s separation of powers,’ Andrew Morris, senior litigation counsel at NCLA, said in a statement announcing the suit. The complaint seeks a court order declaring the tariffs unconstitutional and finding that they were adopted in violation of US administrative rules.”

(2) Other business groups are considering similar challenges. Politico reports: “At issue is a nearly-50-year-old law, the International Emergency Economic Powers Act, that Trump is citing to impose both the duties on China and the global ‘reciprocal tariffs’ he announced this week. The 1977 law gives the president broad authority to respond to a national emergency. But Trump is the first president to use it to impose tariffs, which is a power the U.S. Constitution assigned to Congress.”

Might the Fed come to the rescue and provide enough monetary easing to offset the deflationary consequences of Trump’s tariffs? On Friday, Trump posted the following on Truth Social: “This would be a PERFECT time for Fed Chairman Jerome Powell to cut Interest Rates. He is always ‘late,’ but he could now change his image, and quickly. Energy prices are down, Interest Rates are down, Inflation is down, even Eggs are down 69%, and Jobs are UP, all within two months - A BIG WIN for America. CUT INTEREST RATES, JEROME, AND STOP PLAYING POLITICS!”

Also on Friday, shortly after Trump’s plea, Powell told business journalists in Arlington, Virginia, that the Fed is in no hurry to cut the federal funds rate. He said the Fed faces a “highly uncertain outlook” because of Trump’s reciprocal tariffs. He also said that the tariffs announced were “significantly larger than expected.” In his prepared remarks, Powell stated: “Our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem. … We are well positioned to wait for greater clarity before considering any adjustments to our policy stance. It is too soon to say what will be the appropriate path for monetary policy.”

In other words, “Fuhgeddaboudit” was Powell’s response to Trump.

That was also Powell’s message to the financial markets. Nevertheless, by the end of trading on Friday, the financial futures market signaled that it expects two to three 25bps rate cuts over the next six months and four to five rate cuts over the next 12 months.

▌View Related Live Charts: US - FedWatch Interest Rate Projections

▌View Related Live Charts: US - FedWatch Interest Rate Projections

Trump’s Tariffs II: Nero Golfs.

In his CNN interview Saturday morning, Navarro claimed that thanks to Trump’s policies, the price of oil has dropped sharply, thus reducing the price of gasoline.

▌View Related Live Charts: Brent Crude Oil

▌View Related Live Charts: US - AAA Daily National Average Gasoline Prices

He also noted that bond yields have dropped, causing mortgage rates to decline.

▌View Related Live Charts: US - 10Y/2Y Treasury Yield Spread vs. Treasury Price

▌View Related Live Charts: US - 10Y Treasury Yield vs. Mortgage

He was making the debatable claim that the pain the tariffs are causing for stock investors has been more than offset by the gain of lower gasoline prices and mortgage rates. In addition, he stated that a few companies and countries have recently committed to spend trillions of dollars on capital investments in the US.

The Great Crash during the Great Depression was also accompanied by plunging commodity prices and interest rates. So it is hard to take comfort from last week’s drop in commodity prices and interest rates. The administration can’t take any credit for falling commodity prices and interest rates if the reason they are falling is that the administration’s tariff policies are causing a recession! Capital spending always declines during recessions even if spending commitments were made during good times.

The biggest risk to the economy currently, following last week’s stock market rout, is that the resulting negative wealth effect depresses consumer spending:

(1) Total equity market capitalization.

Data compiled by the Fed show that the total value of stocks traded in the US at the end of 2024 was $93 trillion.

▌View Related Live Charts: MM US Stock Fundamental Index

At the end of Q1-2025, the total value of the S&P 500 was $50 trillion. So a 10% to 20% drop in this stock index would amount to a loss of $5 trillion to $10 trillion just in the S&P 500. That could have a significant negative wealth effect on US consumer spending, especially by retired and retiring Baby Boomers.

(2) Who owns US equities?

Of the $93 trillion in total equities, American households directly held $38 trillion at the end of Q4-2024. Mutual funds and ETFs held $24 trillion. Institutional investors including life insurance companies, private pension funds, and federal, state & local government retirement funds held $10.2 trillion. The rest of the world held $16.5 trillion.

(3) Households & Baby Boomers.

The Fed also compiles data for the net worth of the household sector excluding nonprofit organizations. At the end of 2024, households held $46.8 trillion in corporate equities and mutual funds.

The Baby Boomers accounted for more than half of that at $25.2 trillion.

At the end of last year, households held a record $15.2 trillion in IRAs.

Altogether, equities as a share of the assets held by households (including NPOs) rose to a record 43.5% during Q4-2025.

This means that they are more exposed to a negative wealth effect from falling stock prices. That’s what is happening on Main Street.

(4) ‘Nero fiddles as Rome burns.’ On Friday, the President went to Trump International Golf Club in West Palm Beach, before attending a fundraising dinner for a super PAC that backs Trump, MAGA Inc. On Saturday, he golfed at his course in Jupiter, where the Senior Club Championships are taking place. The White House reported that Trump “won his second round matchup of the Senior Club Championship ... and advances to the Championship Round tomorrow.”

The President wasn’t negotiating trade deals this weekend. He was too busy relaxing on the links.

Trump’s Tariffs III: Stress Testing a Resilient Economy.

The plunge in stock prices since Liberation Day increases the odds that the resulting negative wealth effect will depress consumer spending, which increases the odds of a recession, which is, in turn, depresses stock prices. The odds of a recession according to Polymarket.com rose to 60% at the end of Friday.

▌View Related Live Charts: US - Probability of Recession in A Year (10Y-3M Model)

It was at 42% on April 1.

We raised our subjective probability of a recession this year from 20% to 35% on March 5, and from 35% to 45% on March 31. Along the way, we also slashed our year-end target for the S&P 500 from 7000 to 6000 and cut our projection for 2025 S&P 500 earnings per share from $285 to $260. We also lowered our real GDP growth rate projection for this year from 2.5% to 3.0%, then down to 1.5%.

We expected Liberation Day to bring trouble. So for now, we aren’t changing our outlook or our odds of a recession. Call us delusional optimists, but we aren’t ready to bet against the resilience of the US economy in general or its consumers in particular. Of course, our big assumption is that Trump’s tariff nightmare will go away sooner rather than later, one way or another.

Meanwhile, let’s review the latest signs of the economy’s resilience; we acknowledge that they might be the last ones for a while if the nightmare persists:

(1) Employment. We anticipated a strong rebound in March employment from the depressed gains during January and February, which we attribute to colder-than-normal weather. Nonfarm payrolls rose 228,000 during March.

▌View Related Live Charts: US - Nonfarm Payrolls by Sector (Monthly Change)

Private services-providing industries increased their payrolls by 197,000. Aggregate weekly hours worked rose to a record 4.6 billion.

(2) Retail sales.

We also expect to see a rebound in March retail sales when it’s reported on April 16. We already know that auto sales jumped 11% m/m during March to 17.8 million units (saar), the highest since April 2021.

▌View Related Live Charts: US - Retail Sales vs. Car Sales

Some of that rebound undoubtedly reflected buying in advance of price increases resulting from Trump’s tariffs. April’s sales should also be very strong. But after that, sales could go over a cliff unless Tariff Man changes his mind.

Vivianna speaks at SEMICON TAIWAN's Market and Industry Trend Forum, Sept 1. Code [88MXQ] for ticket discount.

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »