Executive Summary:

Will all the Trump turmoil deepen the recent stock market correction into a bear market? Very few bear markets have occurred without accompanying recessions. If no recession looms, today’s historically stretched valuations could be sustained, Dr Ed says. But the Trump factor is unpredictable, and a trade war could cause a recession. Would Trump pivot before that point, pressured by the Stock Market Vigilantes? … Read on for Ed’s balanced assessment of both the bear and bull market cases. … And an unsettling question for the future: Might the “Roaring 2020s” give way to a repeat of the 1930s, “The New Global Disorder of the 2030s”? It’s all up to Trump. … Check out the accompanying chart collection.

Strategy I: The Valuation Problem.

Last Thursday, I visited with some of our accounts in Connecticut. They seemed remarkably relaxed that day as the S&P 500 fell into correction territory. Many of them are seasoned institutional investors and have been through lots of corrections and bear markets. Everyone attributed the selloff to Trump Tariff Turmoil 2.0.

The bulls still believe (hope) that President Donald Trump is using tariffs as a bargaining tool to negotiate lower tariffs with America’s major trading partners. Some of them predict that if that’s not the case, then Trump will back off in response to political pressure to do so from lots of constituencies that stand to be harmed by a trade war. He might also back off if the stock market continues to tank. The bears warn that by the time Trump ever would relent, the economy would be in a consumer-led recession and the stock market surely would be in a bear market.

We remain bullish, but less so. On Wednesday, March 5, Eric, Debbie, and I raised the odds of a bearish scenario from 20% to 35%. That might entail an outright recession or a period of stagflation. On March 9, we wrote: We can’t rule out the possibility that a bear market started on February 20, the day after the S&P 500 rose to a record high. On March 13, we lowered our year-end 2025 S&P 500 target from 7000 to 6400.

We continue to bet on the resilience of the consumer, the economy, and corporate earnings, but we reckon that heightened recession fears will weigh on valuation multiples. We acknowledge that the risks of a recession and a bear market might continue to increase. It all depends on the often-unpredictable President, who frequently—and proudly—has referred to himself as “Tariff Man,” reflecting his strong support for protectionist trade policies.

We all know that the S&P 500 forward P/E and P/S are stretched by historical standards.

▌View Related Live Charts: US - S&P 500 - Forward PE Ratio

▌View Related Live Charts: US - S&P 500 - Forward PE Ratio

The latter, which is simply a weekly version of the Buffett Ratio, rose to a record high of 3.04 on December 4.

▌View Related Live Charts: US - Buffett Indicator

▌View Related Live Charts: US - Buffett Indicator

It was back down to 2.75 last week, which is still very high. The forward P/E ratio remained below its previous two cyclical highs because the rising forward profit margin boosted earnings relative to revenues.

Nevertheless, the forward P/E was high at 20.2 last week, though down from a recent peak of 22.3 during the December 6 week.

We’ve argued that high valuation multiples might be sustainable if there is no recession in sight. Since the S&P 500 peaked at a record high on February 19, concerns about a recession caused by Trump's tariffs have been mounting, as we acknowledged by raising our subjective odds of a recession. Nevertheless, we didn’t change our optimistic outlook for forward earnings.

But we did lower our range for the forward P/E from 18-22 to 18-20.

The Nasdaq, which peaked at a record high on December 16, fell into correction territory (down 10%-20%) on March 6.

▌View Related Live Charts: NASDAQ Composite Index

▌View Related Live Charts: NASDAQ Composite Index

It is down 12.0% through Friday. The S&P 500 fell into correction territory last Thursday and was down 8.2% from its record peak on Friday.

Corrections occur when the stock market starts to discount a recession that doesn’t occur. It is almost always attributable to a drop in the forward P/E, while forward earnings continue to rise (or at least don’t fall). A bear market (down 20% or more) typically occurs when a recession happens, sending both the valuation multiple and earnings expectations tumbling. Only a few bear markets have occurred when no recession unfolded (i.e., in 1962, 1987, and 2022).

Now let’s turn to the case for a bear market followed by the case for a resumption of the bull market following the latest corrections in the Nasdaq and the S&P 500.

Strategy II: The Bear Case.

The preliminary Consumer Sentiment Index (CSI) survey for March supports the bear case in which consumers reduce their spending, causing a recession. At the same time, higher inflation prevents the Fed from lowering interest rates. The CSI during the first two weeks of March fell to 57.9, the lowest since November 2022.

▌View Related Live Charts: US - Consumer Confidence

▌View Related Live Charts: US - Consumer Confidence

That’s close to the average trough readings of the CSI during the previous six recessions!

In the latest CSI survey, inflationary expectations over the next year and the next five years spiked up to 4.9% and 3.9%.

In the past, such spikes were usually associated with rapidly rising gasoline prices.

This time, inflationary expectations have been inflamed by fears that tariffs will boost prices because they are akin to sales taxes.

Recently, several consumer-related companies have noted that consumer spending might be starting to flag. Walmart CEO Doug McMillon said “budget-pressured” customers are showing “stressed behaviors,” like buying smaller pack sizes at the end of the month because their “money runs out before the month is gone.” Kohl’s and Dick’s Sporting Goods issued weaker-than-anticipated annual forecasts. Delta, American, and Southwest Airlines cut their Q1 estimates, warning of the impact of a weaker economic backdrop on travel demand.

Here are more arguments for the bear case:

(1) Negative wealth effect.

We’ve been observing that retiring Baby Boomers have accounted for much of the resilience of consumer spending, which was boosted by a very positive wealth effect for many as the value of their homes and stock portfolios appreciated. The risk now is that consumers will retrench because of the negative wealth effect attributable to falling stock prices. The Baby Boomers currently hold a record $25.0 trillion in corporate equities and mutual funds, or 54% of the total.

Falling stock prices could have a significant negative wealth effect on the spending of retired Baby Boomers.

(2) DOGE & employment. Elon Musk reduced Twitter’s workforce by approximately 80% after acquiring the company. The number of employees dropped from around 8,000 to about 1,500. He is now also in charge of the Department of Government Efficiency (DOGE) and has been taking a chainsaw to federal government payrolls, which totaled 3.0 civilian workers in January, before Trump 2.0 started to take effect. On Thursday, federal judges in California and Maryland ordered Trump’s administration to reinstate thousands of probationary federal workers who lost their jobs as part of mass firings carried out at 19 agencies.

Also at risk are jobs at contractors of the federal government. The General Accountability Office reported: “The federal government spends hundreds of billions of dollars each year on contracts, which consume a large portion of the federal budget. In FY 2023 alone, the federal government spent over $750 billion on contracts for a wide variety of goods and services—from cybersecurity software to consulting services to aircraft carriers—that are critical to the success of agency missions.”

(3) Uncertainty & capital spending.

There may be methods behind Trump’s tariffs and federal government job cuts, but they certainly have heightened uncertainty and anxiety about the economic outlook. There’s a strong correlation between the CEO Economic Outlook Index (compiled by the Round Table) and the yearly growth rate in capital spending in nominal GDP.

Policy uncertainty and fears of a trade war are bound to depress business confidence and capital spending. The uncertainty index, compiled by the National Federation of Independent Business in a monthly survey of small business owners, has been very volatile and elevated since Election Day.

▌View Related Live Charts: US - NFIB Small Business Optimism Index

▌View Related Live Charts: US - NFIB Small Business Optimism Index

(4) AI bubble bursting. The Magnificent-7 companies are expected to spend a total of $325 billion on capital expenditures in 2025, $100 billion more than in 2024. This includes $75 billion of spending by Alphabet, $80 billion by Microsoft, $100 billion by Amazon, and $65 billion by Meta Platforms. It is widely assumed that this is mostly for AI infrastructure.

The fear now is that open-source large language models (LLMs) like DeepSeek and Manus, developed in China, require much less powerful semiconductors to operate. If so, then AI capital spending will tumble along with the profit margins on AI systems. Since DeepSeek was introduced on January 24, the Roundhill Magnificent-7 ETF (MAGS) is down 15.4%.

▌View Related Live Charts: Big Tech - Magnificent 7 CapEx (Cumulative Total)

▌View Related Live Charts: Big Tech - Magnificent 7 CapEx (Cumulative Total)

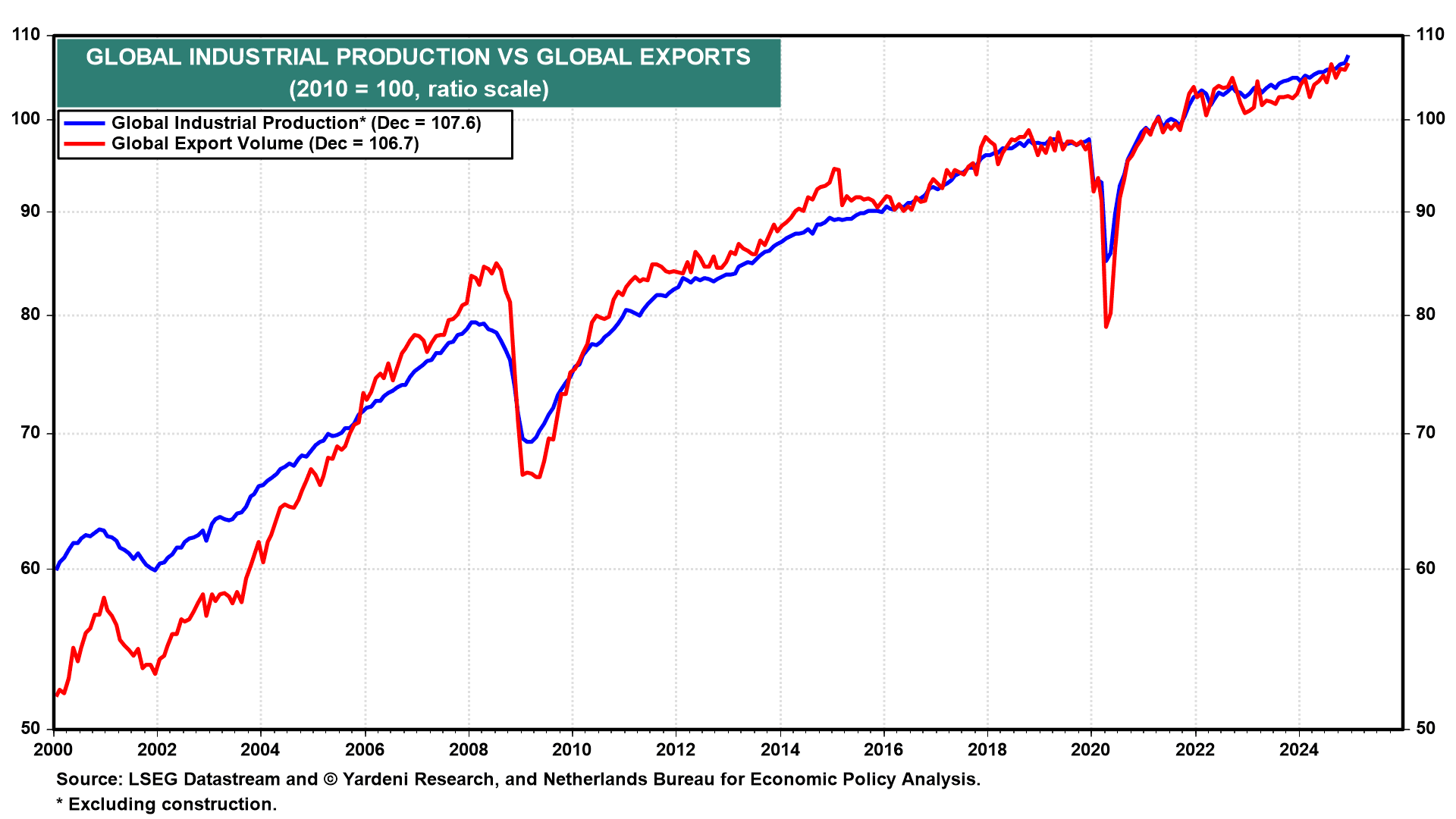

(5) Trade war & global growth.

Globalization has been the main driving force behind global economic prosperity. Global industrial production has been rising along with the volume of global exports for years.

▌View Related Live Charts: World - Global Trade Volume

▌View Related Live Charts: World - Global Trade Volume

Supply chains have become globalized, so products assembled in one country have parts manufactured all over the world.

If Trump’s reciprocal tariffs, which are scheduled to be imposed on April 2, lead to negotiations that result in deals to lower tariffs, that would be a very good outcome. If instead they exacerbate the global trade war, which has already started, that would be very bad.

In February, Trump directed his advisers to come up with new tariff levels that take into account the various trade barriers and other economic approaches employed by America’s trading partners. That includes not only the tariffs that other countries charge on US products but also the subsidies they provide to their domestic industries, their exchange rates, and other measures that the President deems unfair.

That’s fine, but this approach of shooting with reciprocal tariffs first and then talking later might quickly escalate into a trade war with a retaliatory tariffs spiral.

(6) The end of American Exceptionalism. Only a few months ago, American Exceptionalism was widely heralded, including in front-cover stories in the media. Indeed, the October 19, 2024 cover story in The Economist was titled “The Envy of the World.” It was a special report on the American economy. With the benefit of hindsight, that might have been an important contrary indicator, an example of the “front-cover curse” I’ve often mentioned.

Another contrary indicator was the substantial $289.0 billion in net purchases of US equities by private foreign investors through December 2024.

As we have previously observed, foreign net inflows into US equities tend to be large near tops in the US stock market.

If American Exceptionalism has peaked, then it did so on December 24, 2024 when the ratio of the MSCI US stock price index to the MSCI All Country World (ACW) ex-US index (in dollars) peaked.

The ratio has dropped sharply since then, though it remains on the upward trend that started in 2010.

What has certainly been exceptional about the US stock market is its valuation multiple. Its gap with that of the rest of the world has been widening since 2012.

▌View Related Live Charts: MSCI ACWI Forward EPS vs. MSCI ACWI Index

▌View Related Live Charts: MSCI ACWI Forward EPS vs. MSCI ACWI Index

Even now, while the MSCI US’s forward P/E has dropped two percentage points over the past few weeks to 20.7, that’s still well above the 13.8 of the MSCI AWC ex-US.

(7) The Stock Market Vigilantes. The economy is clearly being stress-tested by the turmoil unleashed by Trump’s tariff campaign and rapid-fire cuts in federal payrolls. The immediate impact has been rapid corrections in the Nasdaq and S&P 500. In effect, the Stock Market Vigilantes (SMV) are giving the administration a thumbs down. If this wild bunch forces stock prices into bear market territory, the negative wealth effect could cause a self-fulfilling recession.

The administration seems to be inciting the SMVs to do just that. Trump recently dismissed the significance of the stock market, saying “you can’t really watch the stock market” and “markets are going to go up and they’re going to go down.” Treasury Secretary Scott Bessent (who should know better) also downplayed the recent stock market selloff, calling it “a little bit of volatility over three weeks” that the administration is not concerned about. In effect, they are saying that there is no Trump Put for stock investors. At the same time, Fed officials have said that they are in no rush to provide a Fed Put, which in the past often made significant stock market bottoms.

Strategy III: The Bull Case.

Now for an uplifting change, let’s review the bull case. To an important extent, it hinges on the resilience of the US economy. Over the past three years, the economy has demonstrated its resilience by growing despite widespread forecasts that fueled fears of a recession caused by the significant tightening of monetary policy. The lesson that should have been learned is that the US economy can perform remarkably well despite Washington’s constant meddling with it. Actually, that’s been true for a very long time.

Consider the following:

(1) Resilient consumers.

We continue to monitor the weekly Redbook Research retail sales series, which is highly correlated with the monthly retail sales series compiled by the Census Bureau. The former was up solidly at 5.7% y/y during the March 7 week.

▌View Related Live Charts: US - Retail Sales

▌View Related Live Charts: US - Retail Sales

The growth rate of department store sales, which has been around zero in recent years, rose to 1.5% in the latest week, while discount store sales increased 6.9%.

▌View Related Live Charts: US - Redbook Same-Store Retail Sales Index (YoY)

▌View Related Live Charts: US - Redbook Same-Store Retail Sales Index (YoY)

(2) Resilient labor market.

So far, weekly initial unemployment claims suggest that the labor market remains tight: Claims have stayed around 220,000 since the last week of January, excluding a blip to 242,000 during the week of February 21.

▌View Related Live Charts: US - Initial & Continuing Jobless Claims

▌View Related Live Charts: US - Initial & Continuing Jobless Claims

Separate data for federal government employees’ unemployment claims have spiked during the past two weeks, but to only around 1,600 per week.

Recent surveys of job openings conducted by the Conference Board, the National Federation of Independent Business, and the Bureau of Labor Statistics show that openings remain ample.

(3) No Tech Wreck likely. While cloud computing vendors might need to spend less to increase their capacity to run LLMs as a result of DeepSeek, they will still have to expand their datacenter capacity significantly to process and store more AI-related data.

We don’t think that there is a significant valuation problem in the S&P 500 Communication Services and Information Technology sectors—certainly nothing comparable to the technology bubble of the late 1990s. Together, these sectors account for about 40% of the market capitalization of the S&P 500, matching the peak in late 1999 and early 2000, just before the Tech Wreck. However, there’s more earnings justification this time: Their share of the S&P 500’s forward earnings is currently 35%, well exceeding the 22% peak just before the Tech Wreck.

(4) The Fed Put is on standby. Fed officials have frequently stated that they are in no hurry to lower interest rates. That’s a dovish stance since it implies that they are focusing on lowering the federal funds rate, not raising it or holding it steady. If Trump’s policies show signs of pushing the economy into a recession, the Fed will act quickly to lower interest rates. That assumes, as we do, that inflation remains subdued at just a bit north of the Fed’s target of 2.0%. The Trump Put may be kaput, but the Fed Put remains on standby.

(5) Stock market sentiment is so bad. The Investors Intelligence Bull/Bear Ratio dropped to 0.80 last week. Readings below 1.00 have been strong buying signals in the past, though they can stay below 1.00 for some time before the market clearly bottoms. The AAII Bull/Bear Ratio is also very bearish, which is bullish from a contrarian perspective.

From a sentiment perspective, it is possible that Thursday’s selloff followed by Friday’s rally marked a bottom in the correction. We will be more inclined to call a bottom when we see the stock market move higher on a day or days when Trump blusters about tariffs again, which he did not do on Friday. Any day without a Trump tariff comment is a good day for the market. We know that on April 2 there will be lots of reciprocal tariffs imposed on many more nations by the administration, undoubtedly eliciting lots of comments from Tariff Man.

(6) Bottom line. We repeat ourselves: It all depends on the often-unpredictable President, who frequently—and proudly—has referred to himself as “Tariff Man,” reflecting his strong support for protectionist trade policies.

Strategy IV: RIP, Roaring 2020s?

While there’s lots of uncertainty for now about the short-term outlook for the economy, we remain believers in our Roaring 2020s scenario, which we started to write about in 2019. That call worked out well during the first half of the decade. Along the way, we often were reminded that the Roaring 1920s ended badly because of the Smoot-Hawley Tariff, which was passed in June 1930. Unfortunately, such a scenario could happen again if Trump turns out to be a protectionist and triggers a global trade war.

In other words, we can’t dismiss the possibility that Trump will convert our Roaring 2020s scenario into the New Global Disorder of the 2030s—the analogy being the terrible 1930s.

Before that happens, we would expect lots of pushback from constituencies of Republican congressional representatives clamoring for an end to the tariff turmoil. The Republicans have very narrow majorities in both houses of Congress. They can expect to lose both those majorities if Trump uses tariffs to pursue protectionism, causing increasing retaliatory tariffs and a recession, rather than using them to negotiate freer trade by lowering tariffs in a reciprocal fashion to promote global prosperity.

Executive Summary:

Will all the Trump turmoil deepen the recent stock market correction into a bear market? Very few bear markets have occurred without accompanying recessions. If no recession looms, today’s historically stretched valuations could be sustained, Dr Ed says. But the Trump factor is unpredictable, and a trade war could cause a recession. Would Trump pivot before that point, pressured by the Stock Market Vigilantes? … Read on for Ed’s balanced assessment of both the bear and bull market cases. … And an unsettling question for the future: Might the “Roaring 2020s” give way to a repeat of the 1930s, “The New Global Disorder of the 2030s”? It’s all up to Trump. … Check out the accompanying chart collection.

Strategy I: The Valuation Problem.

Last Thursday, I visited with some of our accounts in Connecticut. They seemed remarkably relaxed that day as the S&P 500 fell into correction territory. Many of them are seasoned institutional investors and have been through lots of corrections and bear markets. Everyone attributed the selloff to Trump Tariff Turmoil 2.0.

The bulls still believe (hope) that President Donald Trump is using tariffs as a bargaining tool to negotiate lower tariffs with America’s major trading partners. Some of them predict that if that’s not the case, then Trump will back off in response to political pressure to do so from lots of constituencies that stand to be harmed by a trade war. He might also back off if the stock market continues to tank. The bears warn that by the time Trump ever would relent, the economy would be in a consumer-led recession and the stock market surely would be in a bear market.

We remain bullish, but less so. On Wednesday, March 5, Eric, Debbie, and I raised the odds of a bearish scenario from 20% to 35%. That might entail an outright recession or a period of stagflation. On March 9, we wrote: We can’t rule out the possibility that a bear market started on February 20, the day after the S&P 500 rose to a record high. On March 13, we lowered our year-end 2025 S&P 500 target from 7000 to 6400.

We continue to bet on the resilience of the consumer, the economy, and corporate earnings, but we reckon that heightened recession fears will weigh on valuation multiples. We acknowledge that the risks of a recession and a bear market might continue to increase. It all depends on the often-unpredictable President, who frequently—and proudly—has referred to himself as “Tariff Man,” reflecting his strong support for protectionist trade policies.

We all know that the S&P 500 forward P/E and P/S are stretched by historical standards.

▌View Related Live Charts: US - S&P 500 - Forward PE Ratio

The latter, which is simply a weekly version of the Buffett Ratio, rose to a record high of 3.04 on December 4.

▌View Related Live Charts: US - Buffett Indicator

It was back down to 2.75 last week, which is still very high. The forward P/E ratio remained below its previous two cyclical highs because the rising forward profit margin boosted earnings relative to revenues.

Nevertheless, the forward P/E was high at 20.2 last week, though down from a recent peak of 22.3 during the December 6 week.

We’ve argued that high valuation multiples might be sustainable if there is no recession in sight. Since the S&P 500 peaked at a record high on February 19, concerns about a recession caused by Trump's tariffs have been mounting, as we acknowledged by raising our subjective odds of a recession. Nevertheless, we didn’t change our optimistic outlook for forward earnings.

But we did lower our range for the forward P/E from 18-22 to 18-20.

The Nasdaq, which peaked at a record high on December 16, fell into correction territory (down 10%-20%) on March 6.

▌View Related Live Charts: NASDAQ Composite Index

It is down 12.0% through Friday. The S&P 500 fell into correction territory last Thursday and was down 8.2% from its record peak on Friday.

Corrections occur when the stock market starts to discount a recession that doesn’t occur. It is almost always attributable to a drop in the forward P/E, while forward earnings continue to rise (or at least don’t fall). A bear market (down 20% or more) typically occurs when a recession happens, sending both the valuation multiple and earnings expectations tumbling. Only a few bear markets have occurred when no recession unfolded (i.e., in 1962, 1987, and 2022).

Now let’s turn to the case for a bear market followed by the case for a resumption of the bull market following the latest corrections in the Nasdaq and the S&P 500.

Strategy II: The Bear Case.

The preliminary Consumer Sentiment Index (CSI) survey for March supports the bear case in which consumers reduce their spending, causing a recession. At the same time, higher inflation prevents the Fed from lowering interest rates. The CSI during the first two weeks of March fell to 57.9, the lowest since November 2022.

▌View Related Live Charts: US - Consumer Confidence

That’s close to the average trough readings of the CSI during the previous six recessions!

In the latest CSI survey, inflationary expectations over the next year and the next five years spiked up to 4.9% and 3.9%.

In the past, such spikes were usually associated with rapidly rising gasoline prices.

This time, inflationary expectations have been inflamed by fears that tariffs will boost prices because they are akin to sales taxes.

Recently, several consumer-related companies have noted that consumer spending might be starting to flag. Walmart CEO Doug McMillon said “budget-pressured” customers are showing “stressed behaviors,” like buying smaller pack sizes at the end of the month because their “money runs out before the month is gone.” Kohl’s and Dick’s Sporting Goods issued weaker-than-anticipated annual forecasts. Delta, American, and Southwest Airlines cut their Q1 estimates, warning of the impact of a weaker economic backdrop on travel demand.

Here are more arguments for the bear case:

(1) Negative wealth effect.

We’ve been observing that retiring Baby Boomers have accounted for much of the resilience of consumer spending, which was boosted by a very positive wealth effect for many as the value of their homes and stock portfolios appreciated. The risk now is that consumers will retrench because of the negative wealth effect attributable to falling stock prices. The Baby Boomers currently hold a record $25.0 trillion in corporate equities and mutual funds, or 54% of the total.

Falling stock prices could have a significant negative wealth effect on the spending of retired Baby Boomers.

(2) DOGE & employment. Elon Musk reduced Twitter’s workforce by approximately 80% after acquiring the company. The number of employees dropped from around 8,000 to about 1,500. He is now also in charge of the Department of Government Efficiency (DOGE) and has been taking a chainsaw to federal government payrolls, which totaled 3.0 civilian workers in January, before Trump 2.0 started to take effect. On Thursday, federal judges in California and Maryland ordered Trump’s administration to reinstate thousands of probationary federal workers who lost their jobs as part of mass firings carried out at 19 agencies.

Also at risk are jobs at contractors of the federal government. The General Accountability Office reported: “The federal government spends hundreds of billions of dollars each year on contracts, which consume a large portion of the federal budget. In FY 2023 alone, the federal government spent over $750 billion on contracts for a wide variety of goods and services—from cybersecurity software to consulting services to aircraft carriers—that are critical to the success of agency missions.”

(3) Uncertainty & capital spending.

There may be methods behind Trump’s tariffs and federal government job cuts, but they certainly have heightened uncertainty and anxiety about the economic outlook. There’s a strong correlation between the CEO Economic Outlook Index (compiled by the Round Table) and the yearly growth rate in capital spending in nominal GDP.

Policy uncertainty and fears of a trade war are bound to depress business confidence and capital spending. The uncertainty index, compiled by the National Federation of Independent Business in a monthly survey of small business owners, has been very volatile and elevated since Election Day.

▌View Related Live Charts: US - NFIB Small Business Optimism Index

(4) AI bubble bursting. The Magnificent-7 companies are expected to spend a total of $325 billion on capital expenditures in 2025, $100 billion more than in 2024. This includes $75 billion of spending by Alphabet, $80 billion by Microsoft, $100 billion by Amazon, and $65 billion by Meta Platforms. It is widely assumed that this is mostly for AI infrastructure.

The fear now is that open-source large language models (LLMs) like DeepSeek and Manus, developed in China, require much less powerful semiconductors to operate. If so, then AI capital spending will tumble along with the profit margins on AI systems. Since DeepSeek was introduced on January 24, the Roundhill Magnificent-7 ETF (MAGS) is down 15.4%.

▌View Related Live Charts: Big Tech - Magnificent 7 CapEx (Cumulative Total)

(5) Trade war & global growth.

Globalization has been the main driving force behind global economic prosperity. Global industrial production has been rising along with the volume of global exports for years.

▌View Related Live Charts: World - Global Trade Volume

Supply chains have become globalized, so products assembled in one country have parts manufactured all over the world.

If Trump’s reciprocal tariffs, which are scheduled to be imposed on April 2, lead to negotiations that result in deals to lower tariffs, that would be a very good outcome. If instead they exacerbate the global trade war, which has already started, that would be very bad.

In February, Trump directed his advisers to come up with new tariff levels that take into account the various trade barriers and other economic approaches employed by America’s trading partners. That includes not only the tariffs that other countries charge on US products but also the subsidies they provide to their domestic industries, their exchange rates, and other measures that the President deems unfair.

That’s fine, but this approach of shooting with reciprocal tariffs first and then talking later might quickly escalate into a trade war with a retaliatory tariffs spiral.

(6) The end of American Exceptionalism. Only a few months ago, American Exceptionalism was widely heralded, including in front-cover stories in the media. Indeed, the October 19, 2024 cover story in The Economist was titled “The Envy of the World.” It was a special report on the American economy. With the benefit of hindsight, that might have been an important contrary indicator, an example of the “front-cover curse” I’ve often mentioned.

Another contrary indicator was the substantial $289.0 billion in net purchases of US equities by private foreign investors through December 2024.

As we have previously observed, foreign net inflows into US equities tend to be large near tops in the US stock market.

If American Exceptionalism has peaked, then it did so on December 24, 2024 when the ratio of the MSCI US stock price index to the MSCI All Country World (ACW) ex-US index (in dollars) peaked.

The ratio has dropped sharply since then, though it remains on the upward trend that started in 2010.

What has certainly been exceptional about the US stock market is its valuation multiple. Its gap with that of the rest of the world has been widening since 2012.

▌View Related Live Charts: MSCI ACWI Forward EPS vs. MSCI ACWI Index

Even now, while the MSCI US’s forward P/E has dropped two percentage points over the past few weeks to 20.7, that’s still well above the 13.8 of the MSCI AWC ex-US.

(7) The Stock Market Vigilantes. The economy is clearly being stress-tested by the turmoil unleashed by Trump’s tariff campaign and rapid-fire cuts in federal payrolls. The immediate impact has been rapid corrections in the Nasdaq and S&P 500. In effect, the Stock Market Vigilantes (SMV) are giving the administration a thumbs down. If this wild bunch forces stock prices into bear market territory, the negative wealth effect could cause a self-fulfilling recession.

The administration seems to be inciting the SMVs to do just that. Trump recently dismissed the significance of the stock market, saying “you can’t really watch the stock market” and “markets are going to go up and they’re going to go down.” Treasury Secretary Scott Bessent (who should know better) also downplayed the recent stock market selloff, calling it “a little bit of volatility over three weeks” that the administration is not concerned about. In effect, they are saying that there is no Trump Put for stock investors. At the same time, Fed officials have said that they are in no rush to provide a Fed Put, which in the past often made significant stock market bottoms.

Strategy III: The Bull Case.

Now for an uplifting change, let’s review the bull case. To an important extent, it hinges on the resilience of the US economy. Over the past three years, the economy has demonstrated its resilience by growing despite widespread forecasts that fueled fears of a recession caused by the significant tightening of monetary policy. The lesson that should have been learned is that the US economy can perform remarkably well despite Washington’s constant meddling with it. Actually, that’s been true for a very long time.

Consider the following:

(1) Resilient consumers.

We continue to monitor the weekly Redbook Research retail sales series, which is highly correlated with the monthly retail sales series compiled by the Census Bureau. The former was up solidly at 5.7% y/y during the March 7 week.

▌View Related Live Charts: US - Retail Sales

The growth rate of department store sales, which has been around zero in recent years, rose to 1.5% in the latest week, while discount store sales increased 6.9%.

▌View Related Live Charts: US - Redbook Same-Store Retail Sales Index (YoY)

(2) Resilient labor market.

So far, weekly initial unemployment claims suggest that the labor market remains tight: Claims have stayed around 220,000 since the last week of January, excluding a blip to 242,000 during the week of February 21.

▌View Related Live Charts: US - Initial & Continuing Jobless Claims

Separate data for federal government employees’ unemployment claims have spiked during the past two weeks, but to only around 1,600 per week.

Recent surveys of job openings conducted by the Conference Board, the National Federation of Independent Business, and the Bureau of Labor Statistics show that openings remain ample.

(3) No Tech Wreck likely. While cloud computing vendors might need to spend less to increase their capacity to run LLMs as a result of DeepSeek, they will still have to expand their datacenter capacity significantly to process and store more AI-related data.

We don’t think that there is a significant valuation problem in the S&P 500 Communication Services and Information Technology sectors—certainly nothing comparable to the technology bubble of the late 1990s. Together, these sectors account for about 40% of the market capitalization of the S&P 500, matching the peak in late 1999 and early 2000, just before the Tech Wreck. However, there’s more earnings justification this time: Their share of the S&P 500’s forward earnings is currently 35%, well exceeding the 22% peak just before the Tech Wreck.

(4) The Fed Put is on standby. Fed officials have frequently stated that they are in no hurry to lower interest rates. That’s a dovish stance since it implies that they are focusing on lowering the federal funds rate, not raising it or holding it steady. If Trump’s policies show signs of pushing the economy into a recession, the Fed will act quickly to lower interest rates. That assumes, as we do, that inflation remains subdued at just a bit north of the Fed’s target of 2.0%. The Trump Put may be kaput, but the Fed Put remains on standby.

(5) Stock market sentiment is so bad. The Investors Intelligence Bull/Bear Ratio dropped to 0.80 last week. Readings below 1.00 have been strong buying signals in the past, though they can stay below 1.00 for some time before the market clearly bottoms. The AAII Bull/Bear Ratio is also very bearish, which is bullish from a contrarian perspective.

From a sentiment perspective, it is possible that Thursday’s selloff followed by Friday’s rally marked a bottom in the correction. We will be more inclined to call a bottom when we see the stock market move higher on a day or days when Trump blusters about tariffs again, which he did not do on Friday. Any day without a Trump tariff comment is a good day for the market. We know that on April 2 there will be lots of reciprocal tariffs imposed on many more nations by the administration, undoubtedly eliciting lots of comments from Tariff Man.

(6) Bottom line. We repeat ourselves: It all depends on the often-unpredictable President, who frequently—and proudly—has referred to himself as “Tariff Man,” reflecting his strong support for protectionist trade policies.

Strategy IV: RIP, Roaring 2020s?

While there’s lots of uncertainty for now about the short-term outlook for the economy, we remain believers in our Roaring 2020s scenario, which we started to write about in 2019. That call worked out well during the first half of the decade. Along the way, we often were reminded that the Roaring 1920s ended badly because of the Smoot-Hawley Tariff, which was passed in June 1930. Unfortunately, such a scenario could happen again if Trump turns out to be a protectionist and triggers a global trade war.

In other words, we can’t dismiss the possibility that Trump will convert our Roaring 2020s scenario into the New Global Disorder of the 2030s—the analogy being the terrible 1930s.

Before that happens, we would expect lots of pushback from constituencies of Republican congressional representatives clamoring for an end to the tariff turmoil. The Republicans have very narrow majorities in both houses of Congress. They can expect to lose both those majorities if Trump uses tariffs to pursue protectionism, causing increasing retaliatory tariffs and a recession, rather than using them to negotiate freer trade by lowering tariffs in a reciprocal fashion to promote global prosperity.

Big Tech earnings week is here! Stay ahead with MacroMicro’s Economic Calendar — track CPI, GDP, and key earnings like Apple & Google all in one place. Check it out »